-

Carbon contracts are needed to ensure that the steel industry’s urgent reinvestment needs are used to further its transformation to climate neutrality.

By compensating for the initially higher costs of climate-friendly production, carbon contracts anticipate the effects of evolving carbon pricing and enable the industry to implement its green investment plans.

-

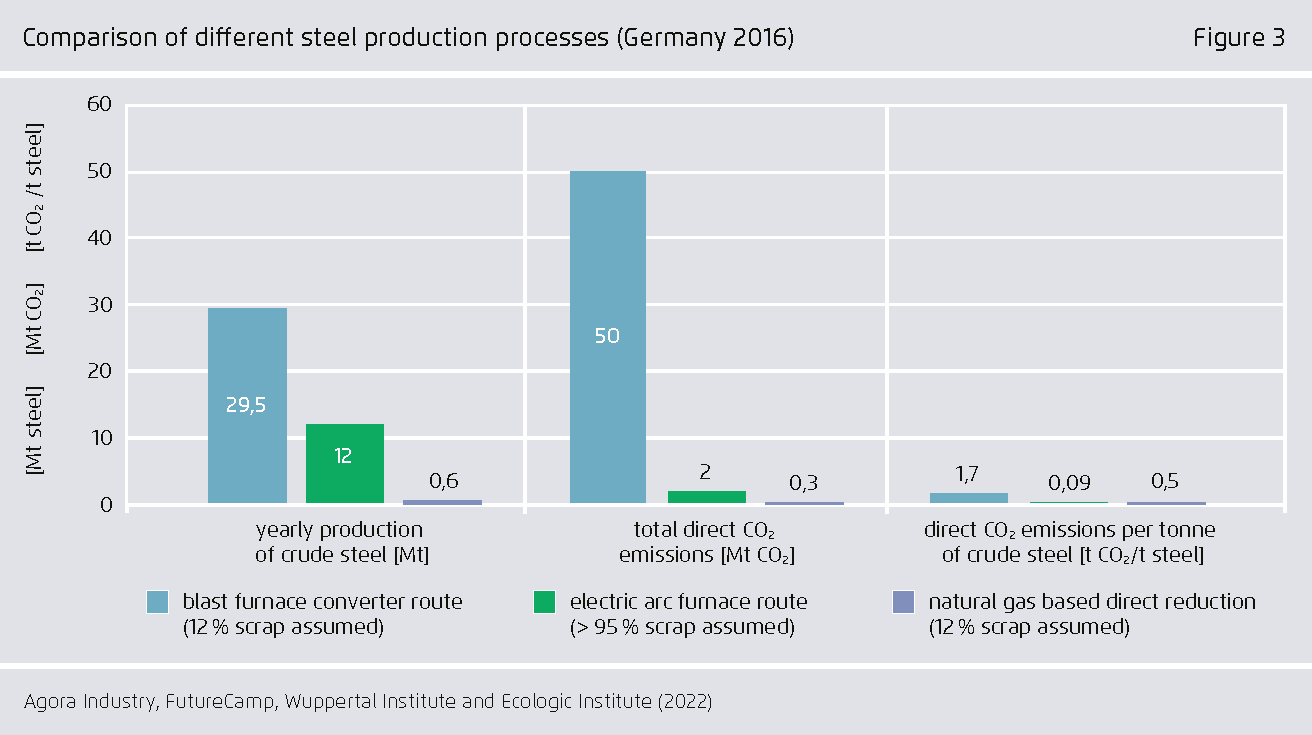

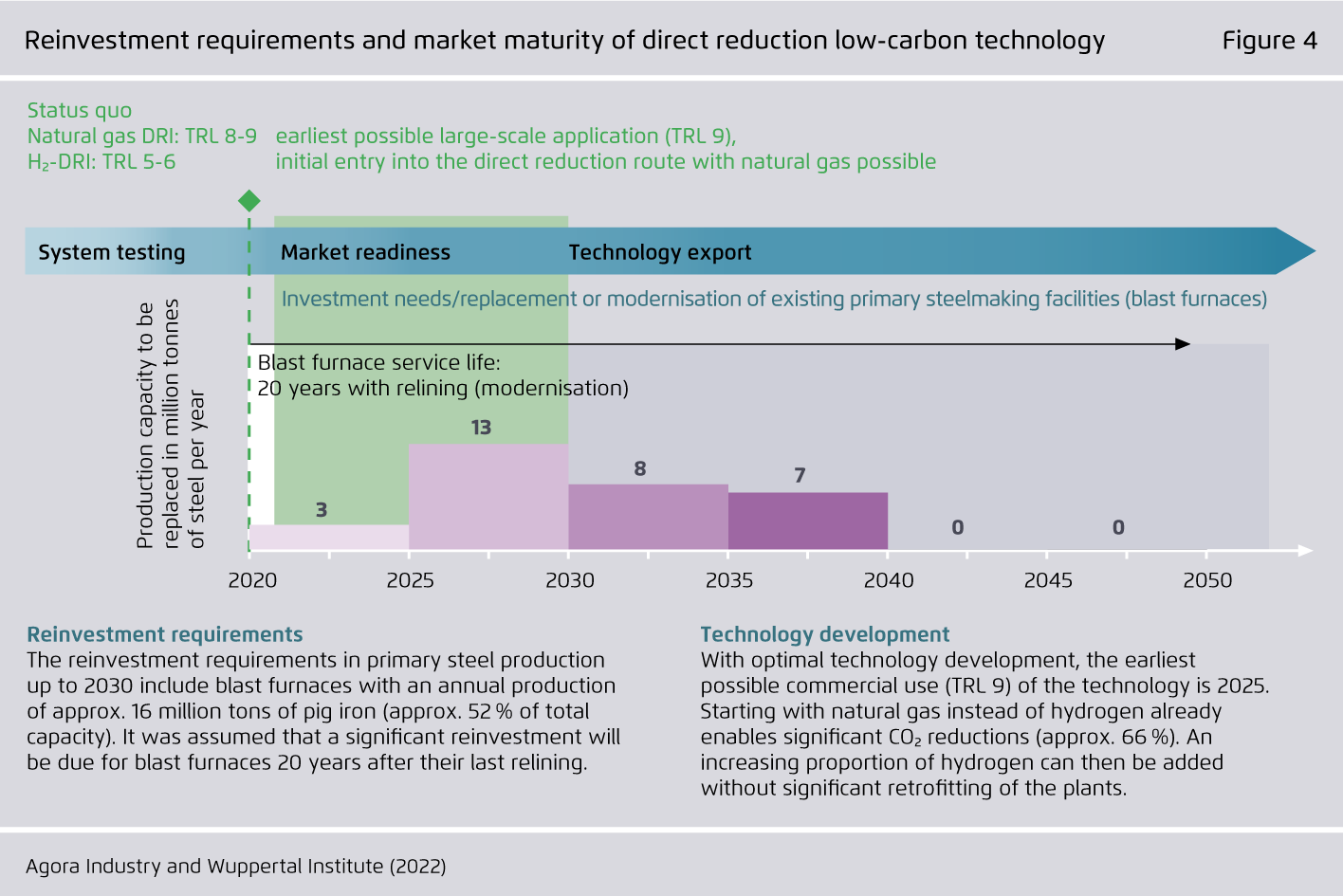

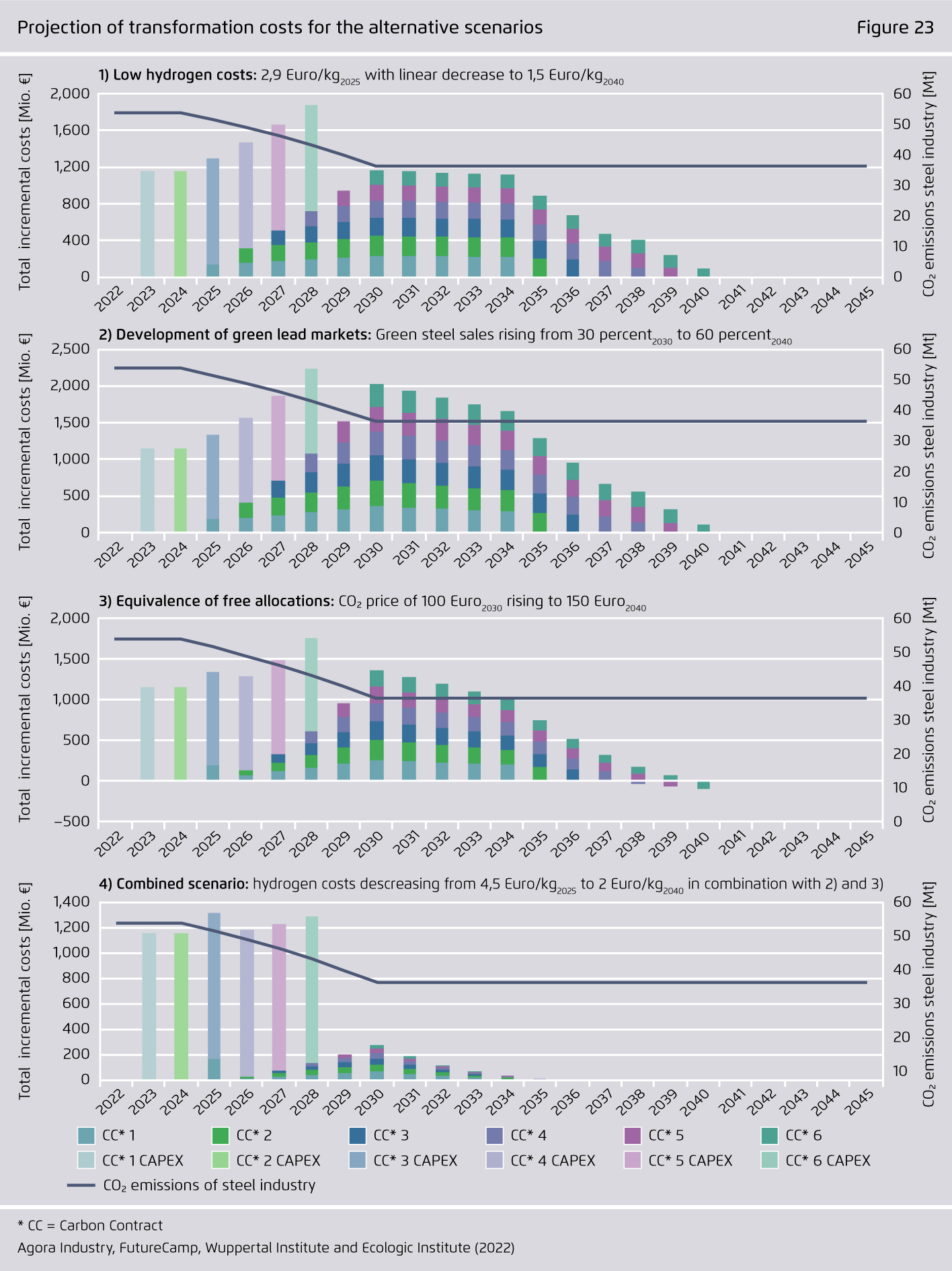

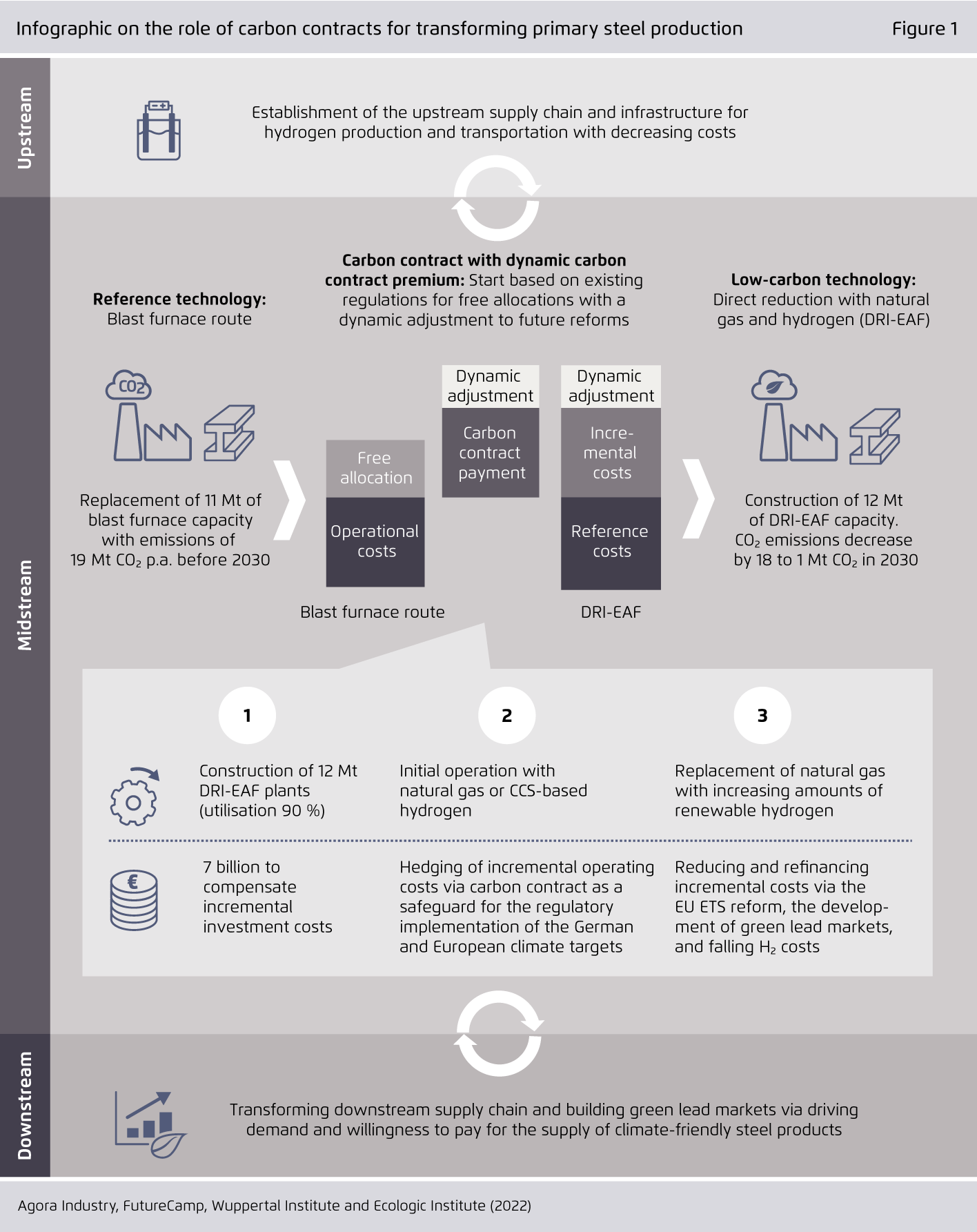

By 2030, Germany must substitute half of its blast furnace capacity. This can be done by increasing steel recycling by 5 million tonnes and building 12 million tonnes of DRI-based production capacity.

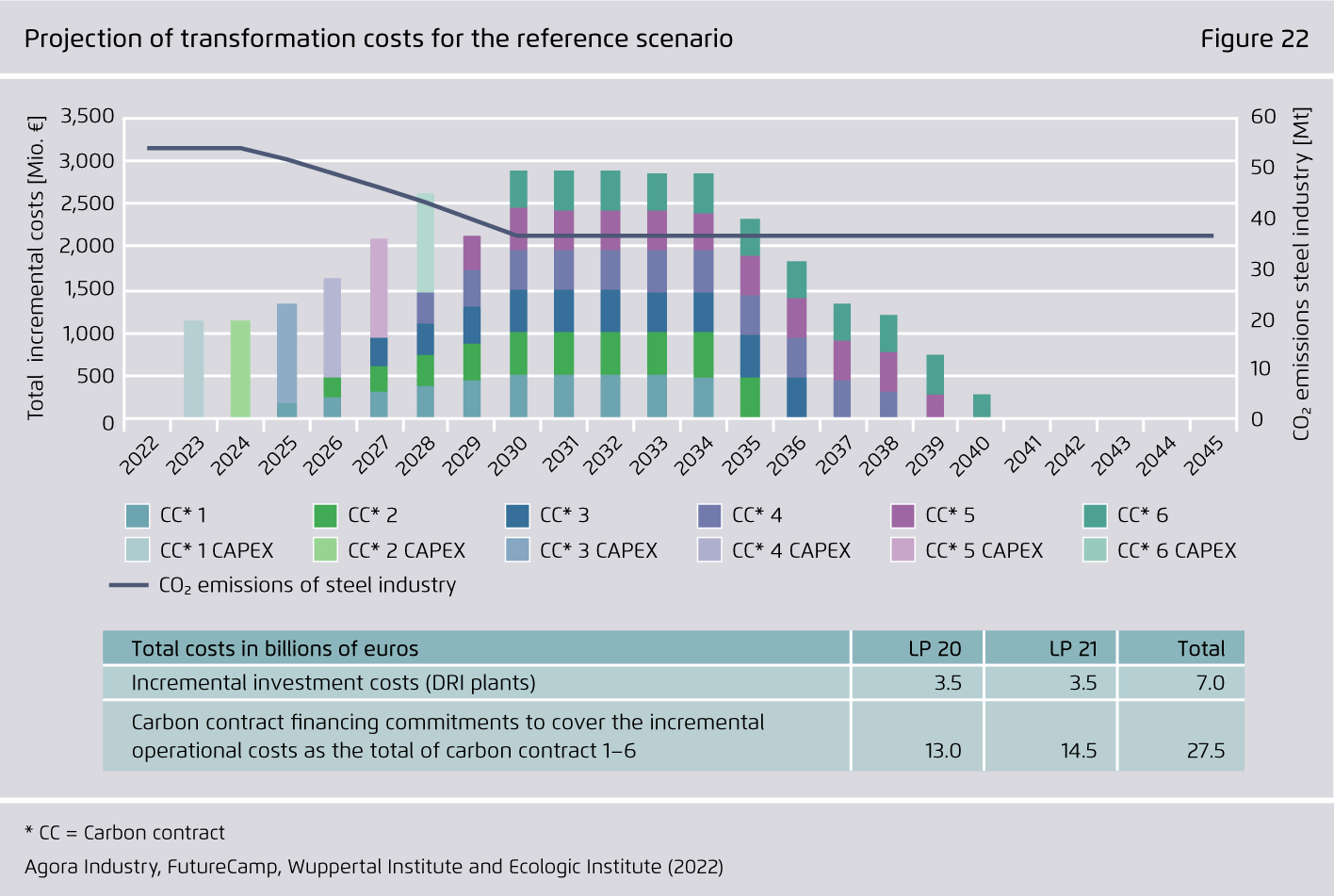

Carbon contracts support this transformation. If appropriately coordinated with other policy measures, the need for financial support is limited to less than 9 billion euros, and green steel can be cost-competitive by 2035.

-

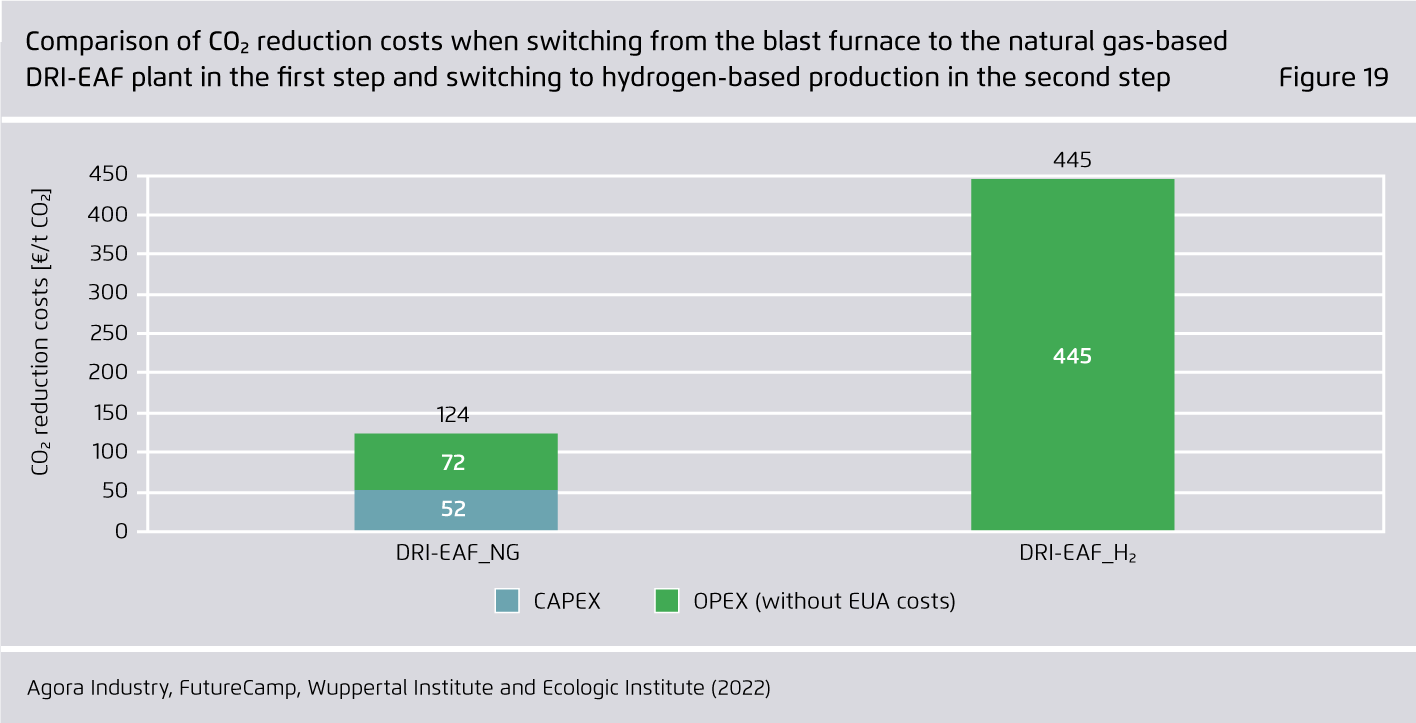

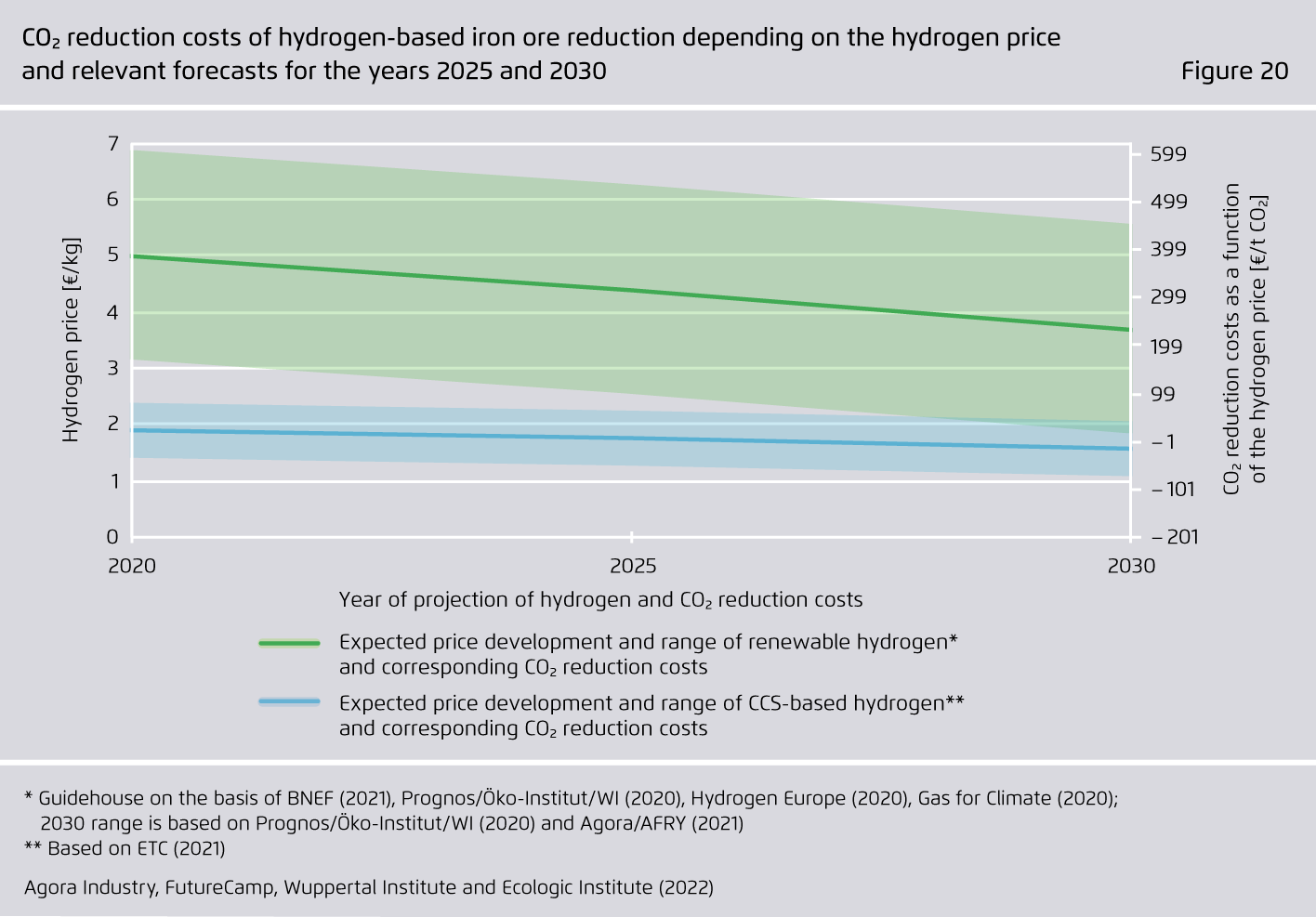

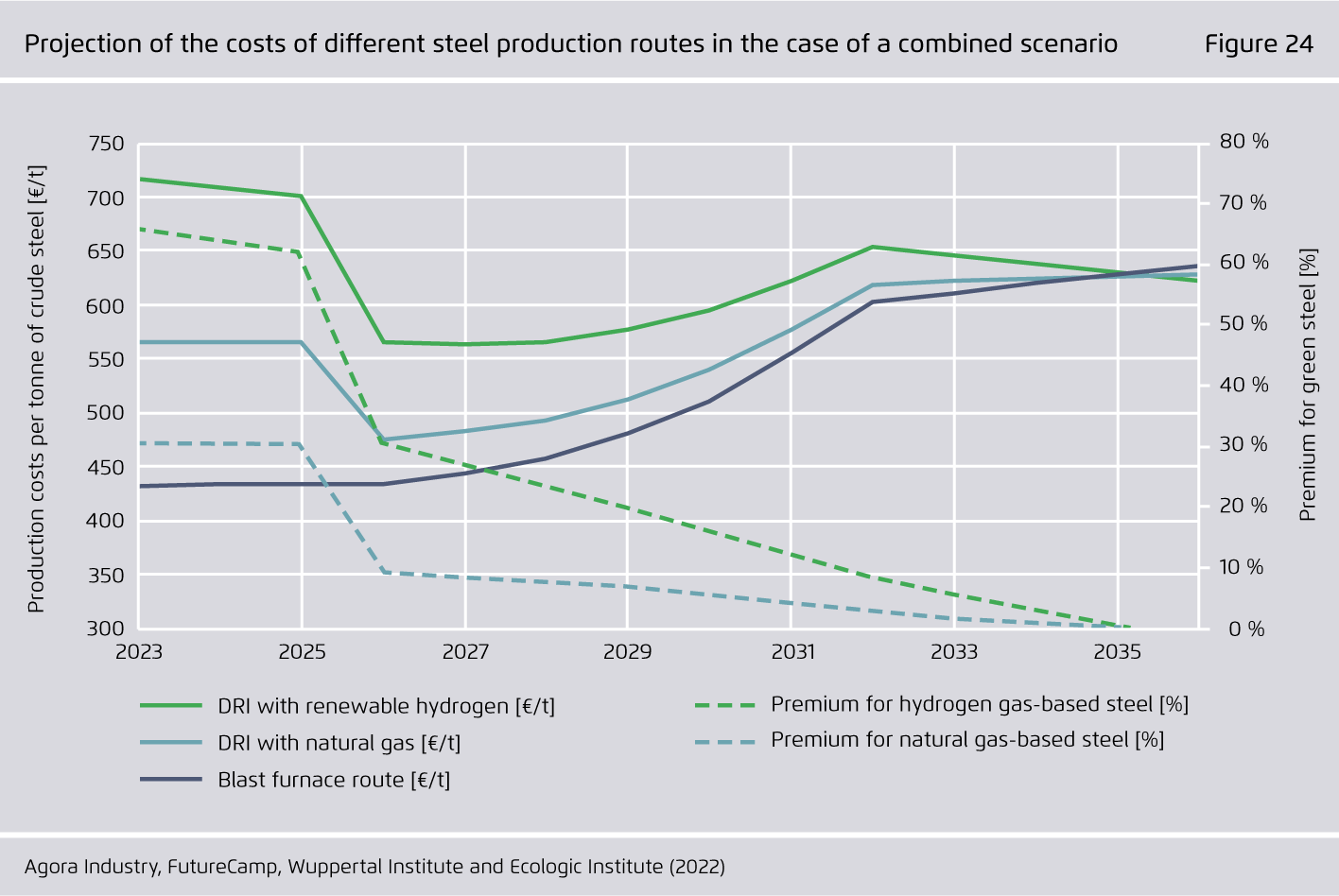

Replacing blast furnaces with DRI plants accelerates the market ramp-up of renewable hydrogen and the development of the necessary infrastructure.

Running them initially on natural gas will enable a rapid reduction in CO2 emissions and provides a back-up for the use of increasing volumes of renewable hydrogen.

-

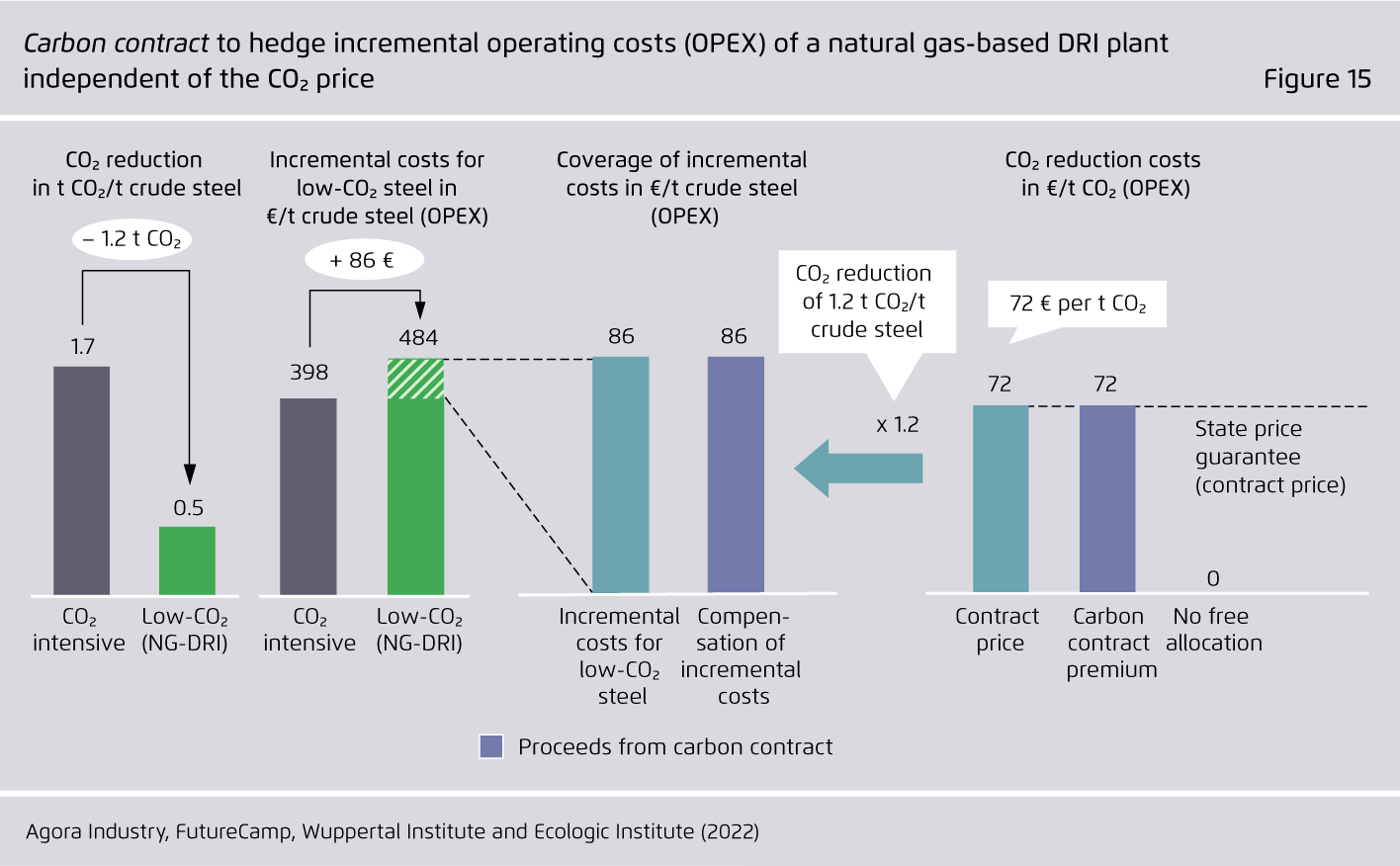

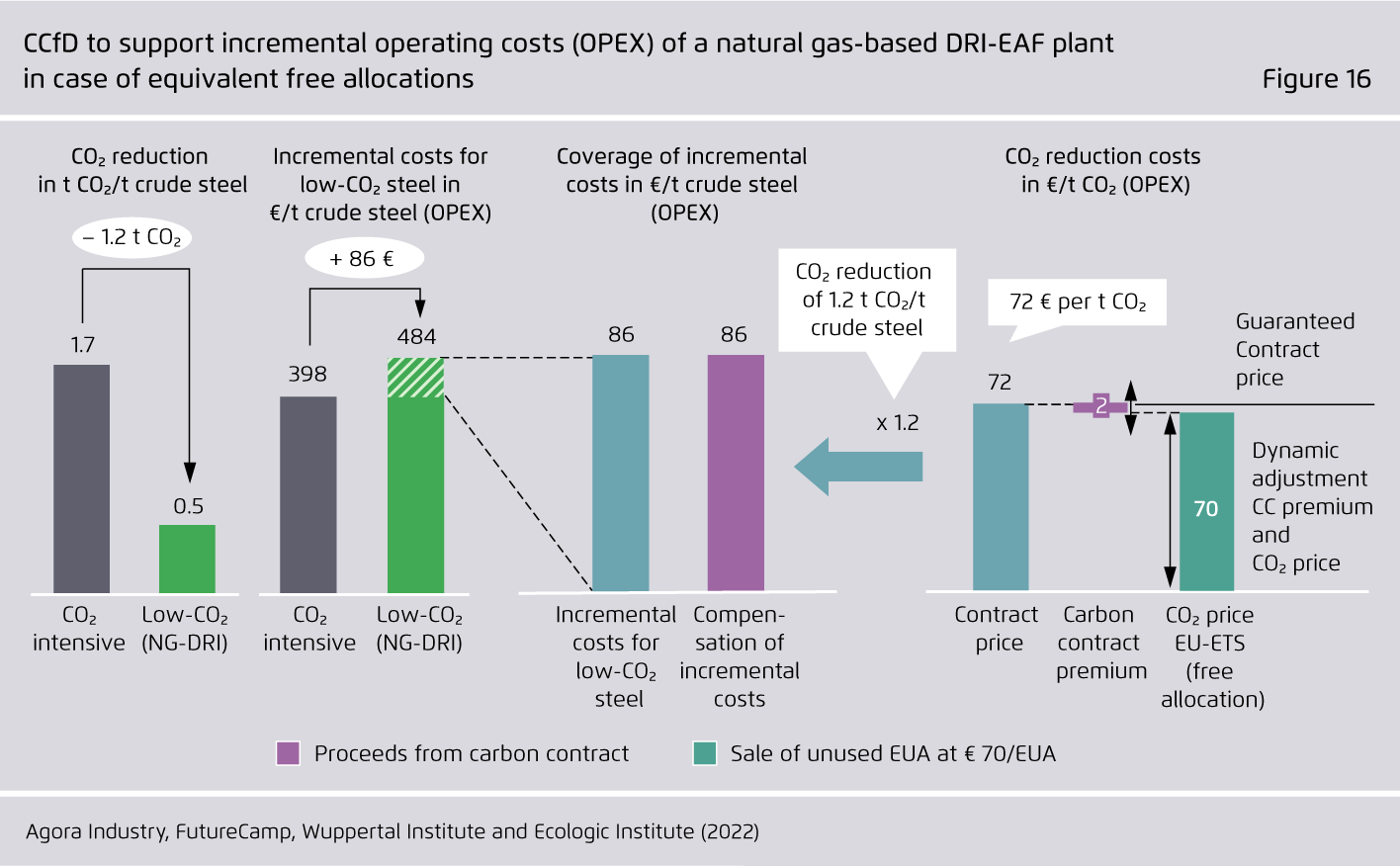

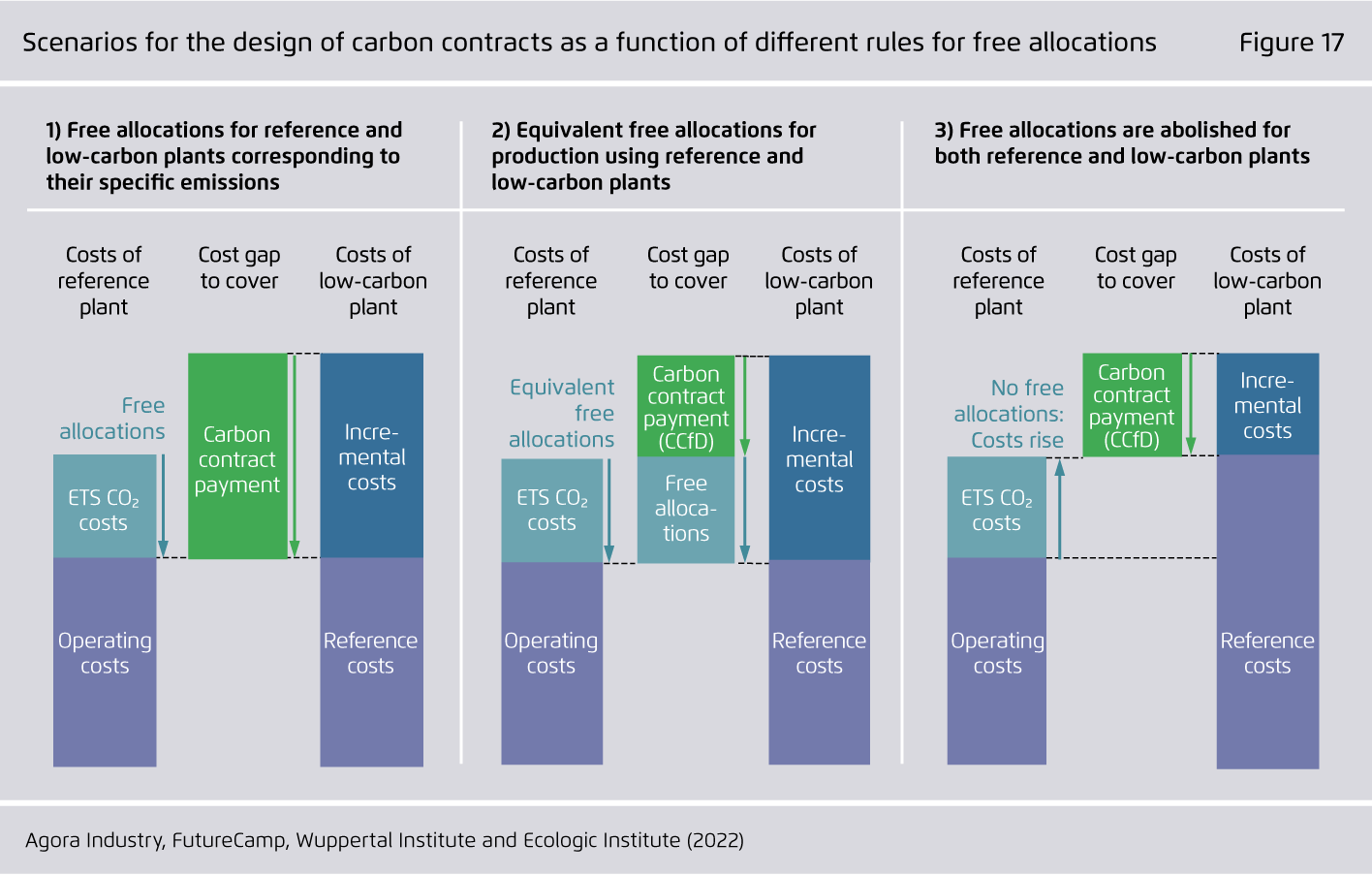

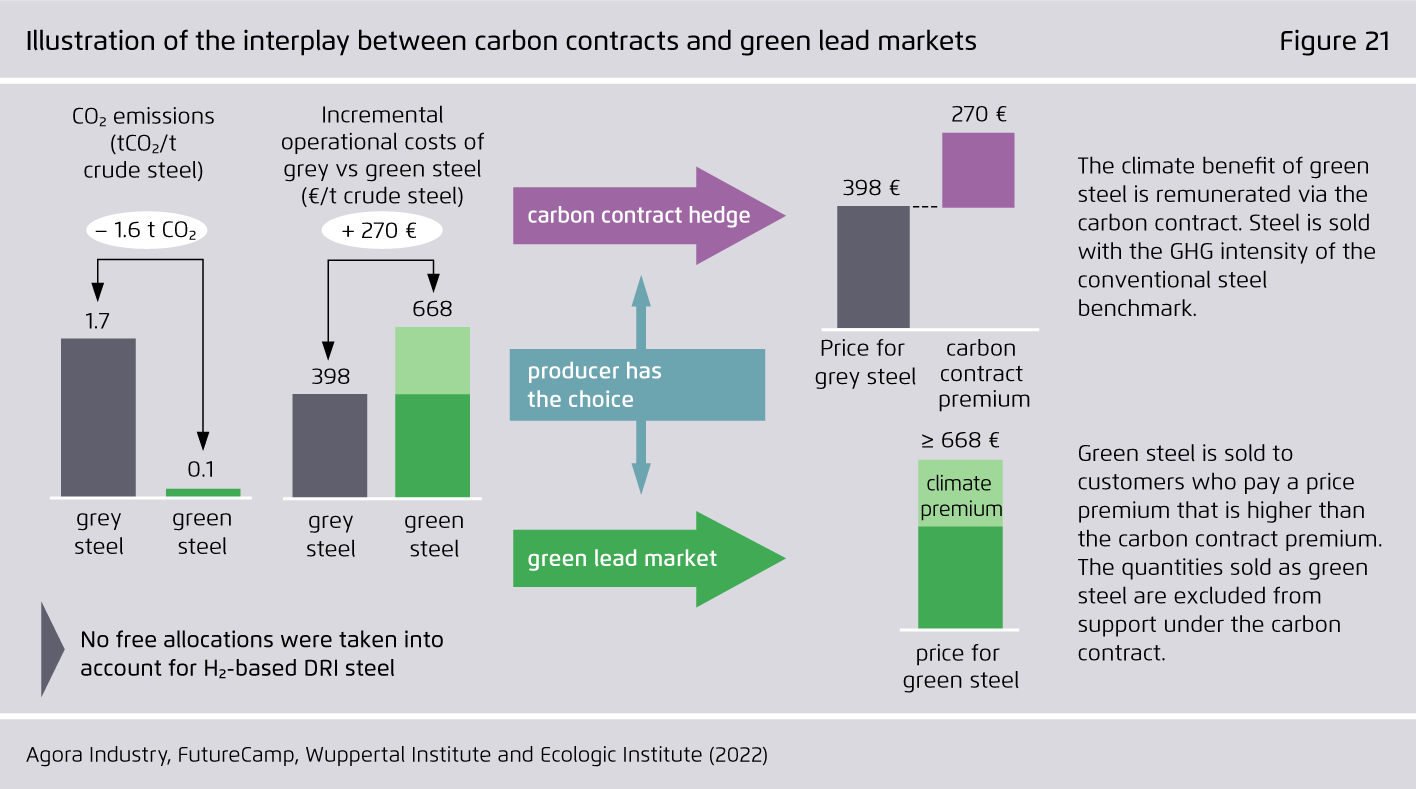

Carbon contracts are a suitable hedging instrument against the incremental costs and uncertainties of climate-friendly steel production in times of crisis.

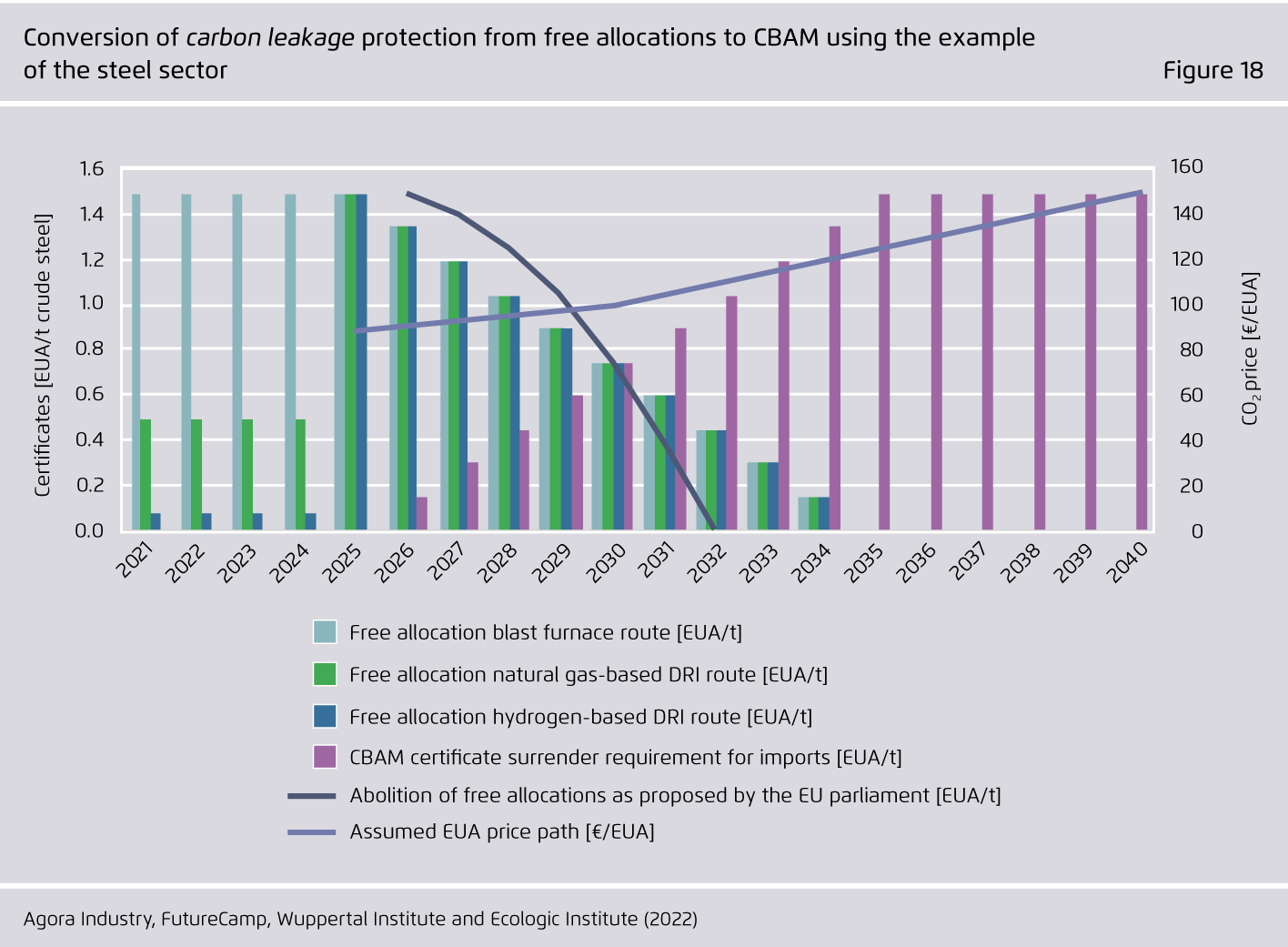

Alongside the rapid implementation of carbon contracts, the EU ETS must be reformed and green lead markets developed so that climate-friendly steel can establish itself as the industry standard.

Transforming industry through carbon contracts (steel)

Analysis of the German steel sector

")

Preface

Steel production is a major source of greenhouse gas (GHG) emissions. In this publication we analyse strategies to reduce these emissions using the example of Germany, which is the world’s eighth largest steel producer and has committed to achieve climate neutrality by 2045. We put forward a plan that would enable the German steel industry to transform its asset base with the course of its natural reinvestment cycle.

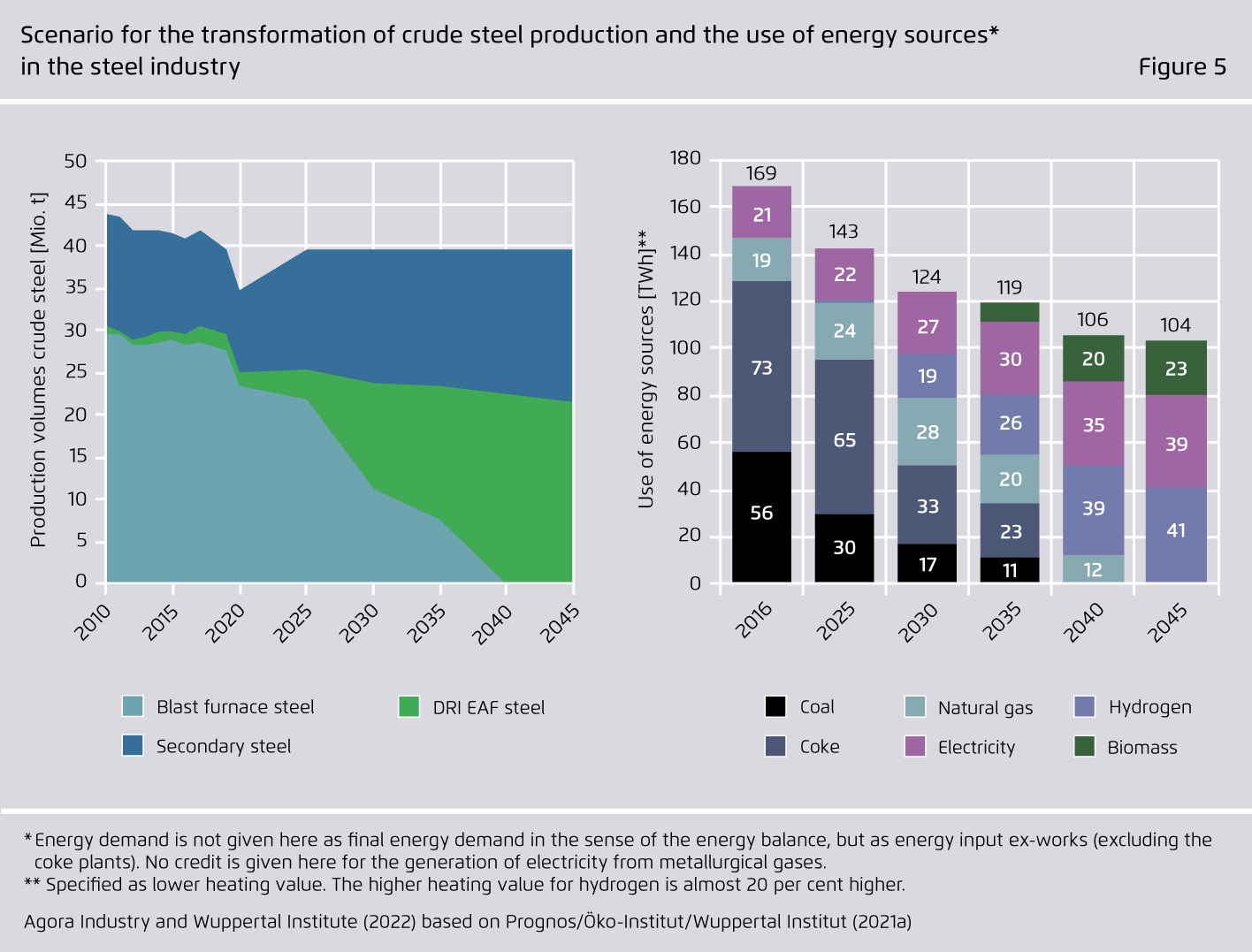

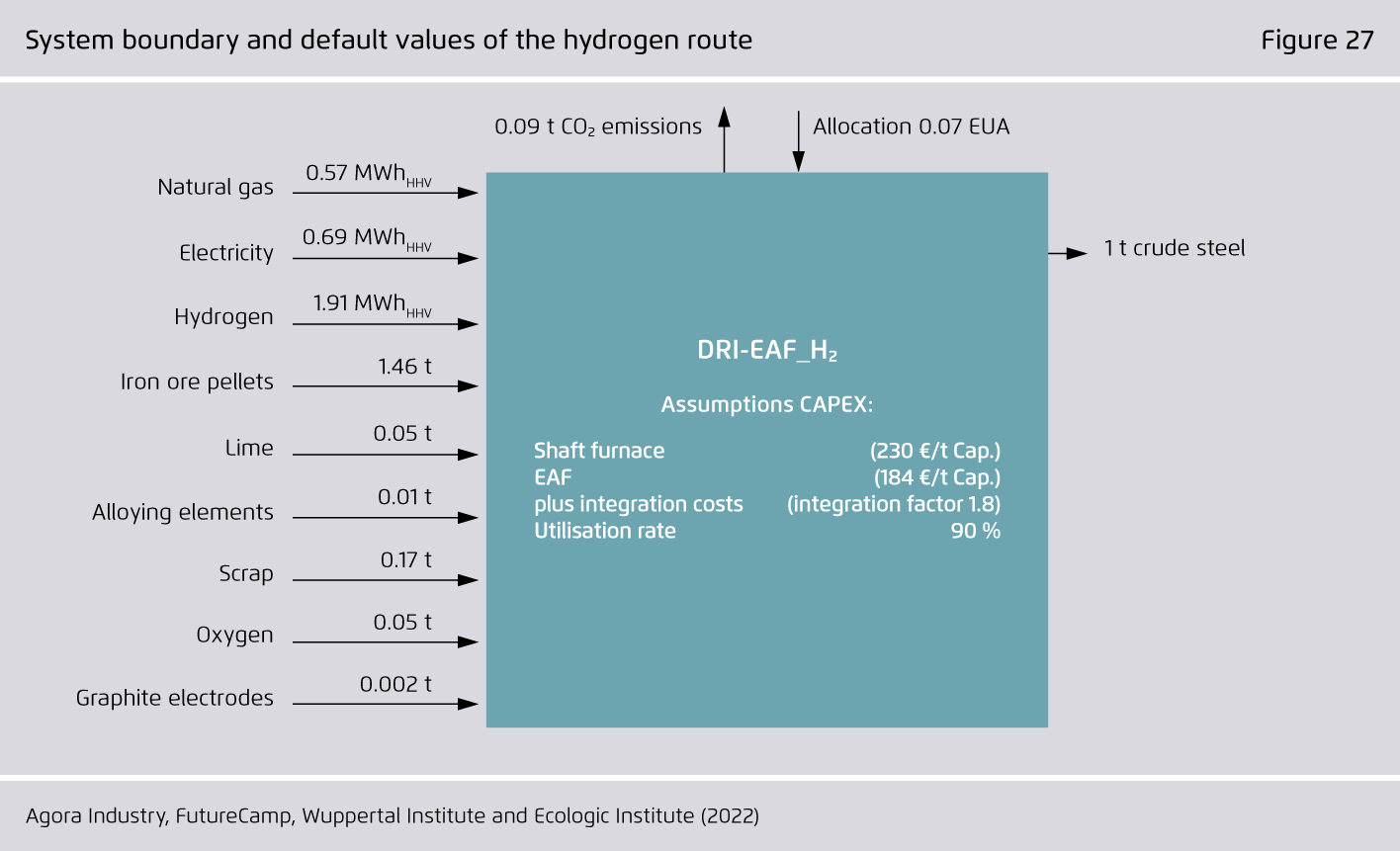

This plan involves substituting coal-based blast furnaces for climate-friendly production of Direct Reduced Iron (DRI) in addition to increasing steel recycling. DRI-technology operates with flexible combinations of natural gas and hydrogen instead of coal and offers significant CO2 emission reduction potential. Due to its flexibility, it can support the development of a renewable hydrogen infrastructure for other sectors.

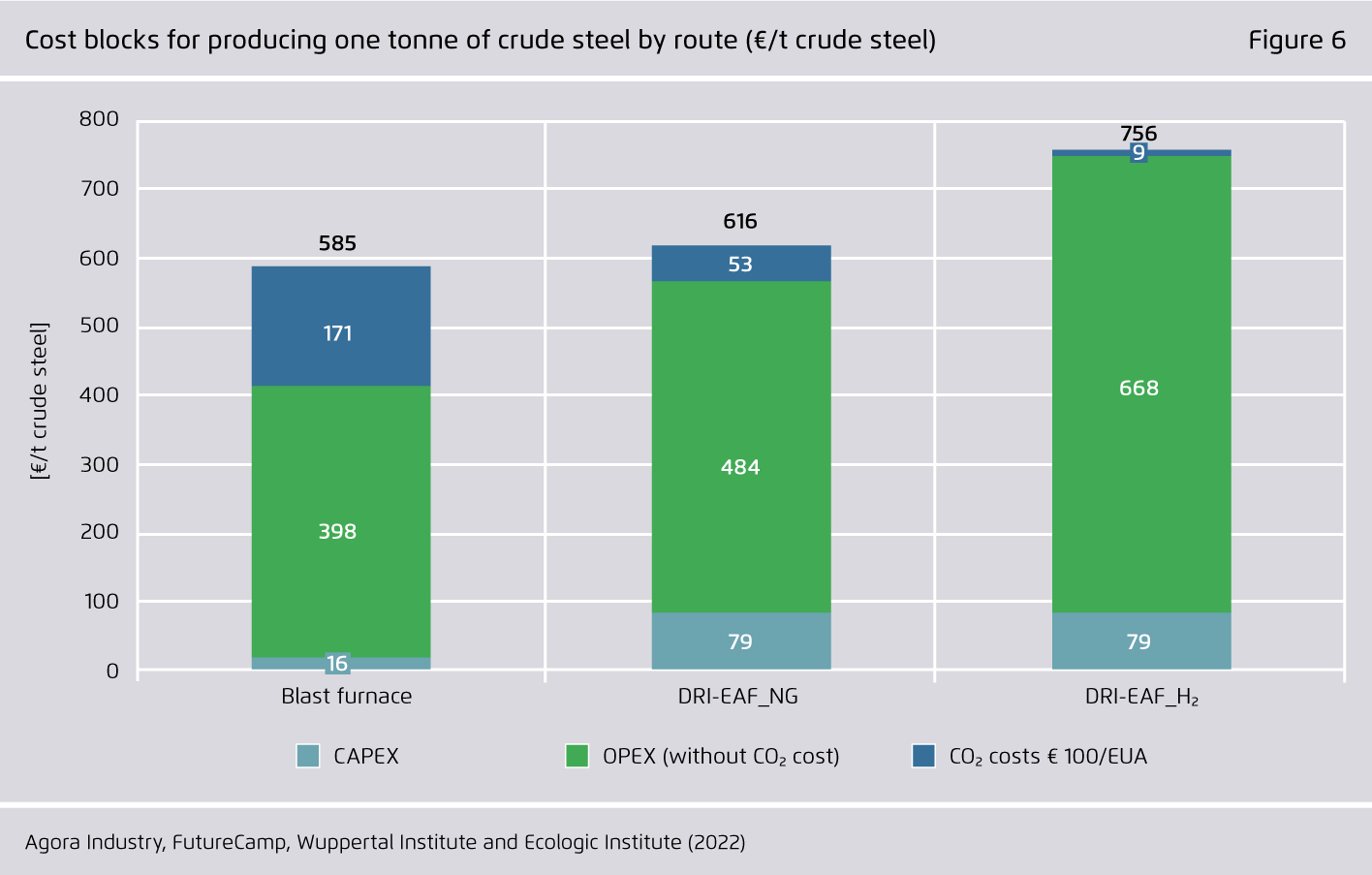

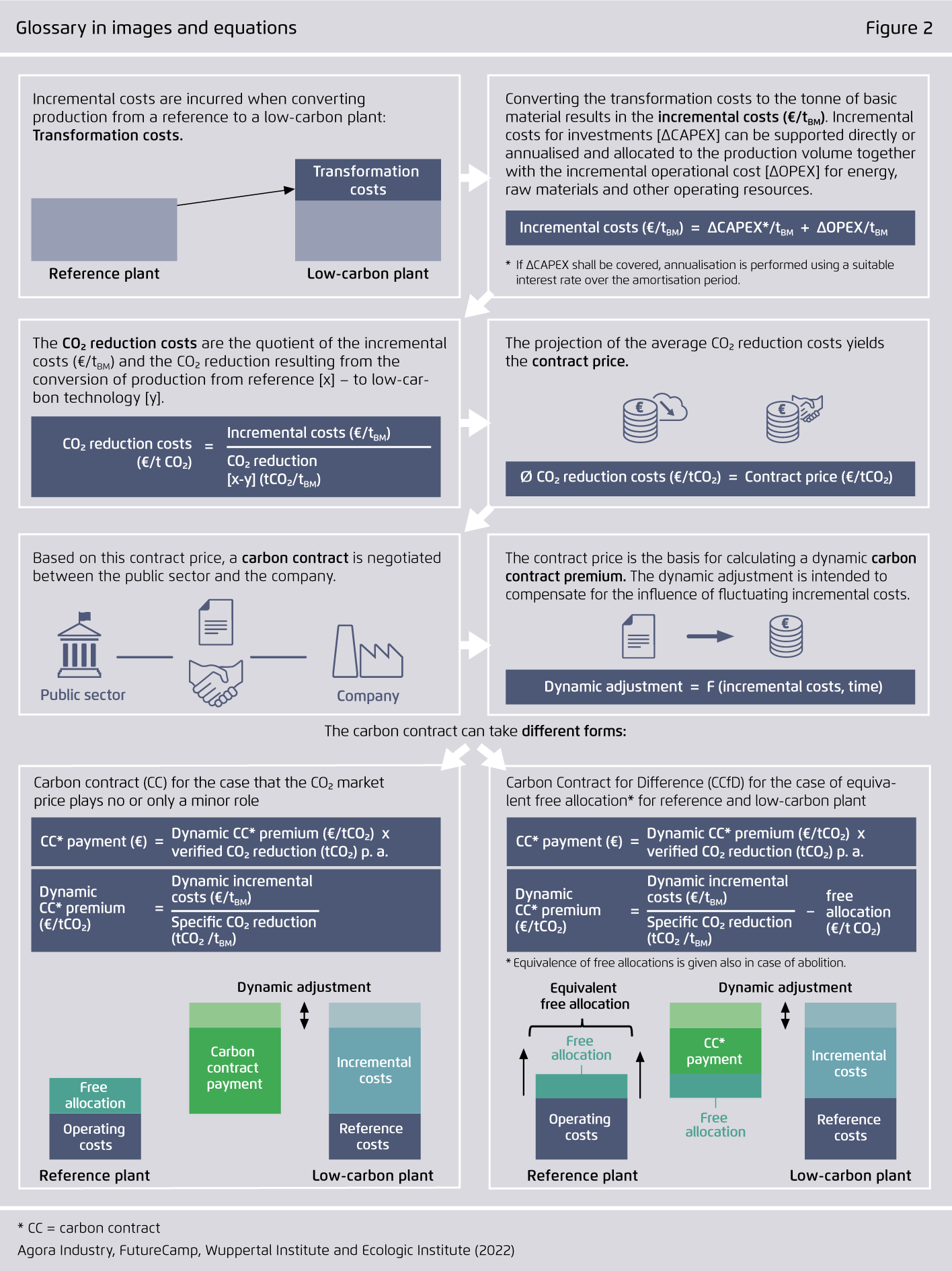

However, building and operating DRI plants is initially more expensive than conventional blast furnaces. Carbon contracts are an instrument that can compensate for such incremental costs until climate-friendly steel is able to compete with GHG-intensive products.

We demonstrate how carbon contracts can be designed as an insurance mechanism against incremental costs arising from various changes: differences in the consumption and price of energy carriers as well as feedstocks, the effect of CO2 prices and the anticipated reforms to the EU ETS. In addition, we discuss how carbon contracts can generate a supply of climatefriendly steel to support and accelerate the growth of market-driven demand.

Our analysis shows that carbon contracts are an effective instrument for accelerating the steel transformation and ensuring the industry’s long-term competitiveness.

Key findings

Bibliographical data

Downloads

-

pdf 3 MB

Transforming industry through carbon contracts

Analysis of the German steel sector

All figures in this publication

Infographic on the role of carbon contracts for transforming primary steel production

Figure 1 from Transforming industry through carbon contracts (steel) on page 9

Share:

Glossary in images and equations

Figure 2 from Transforming industry through carbon contracts (steel) on page 10

Share: