Beyond fossil fuels: unlocking green commodities through de-risked finance

How stronger international cooperation and targeted financing can help build new, competitive low-carbon industries in parallel to phasing out fossil fuels.

-

Karina Marzano Franco

Karina Marzano Franco

The energy transition is as much about building new, competitive low-carbon industries as it is about phasing out fossil fuels. For many oil- and gas-producing economies, green commodities like green iron and ammonia enable cleaner, more resilient and inclusive industrial pathways. As momentum builds ahead of the first ever Conference on Transitioning Away from Fossil Fuels in Santa Marta and the Brazilian COP30 Presidency’s roadmap, we outline how stronger international cooperation and targeted financing can turn this vision into reality.

De-risked finance to make green industry projects bankable

Fossil fuel revenues have long underpinned public budgets, employment and political stability. This dependence underscores the need for viable green alternatives that generate resilient revenue streams, add local value and create future-proof jobs. However, scaling up clean technology projects will require de-risking instruments including concessional and blended finance, loans and guarantees.

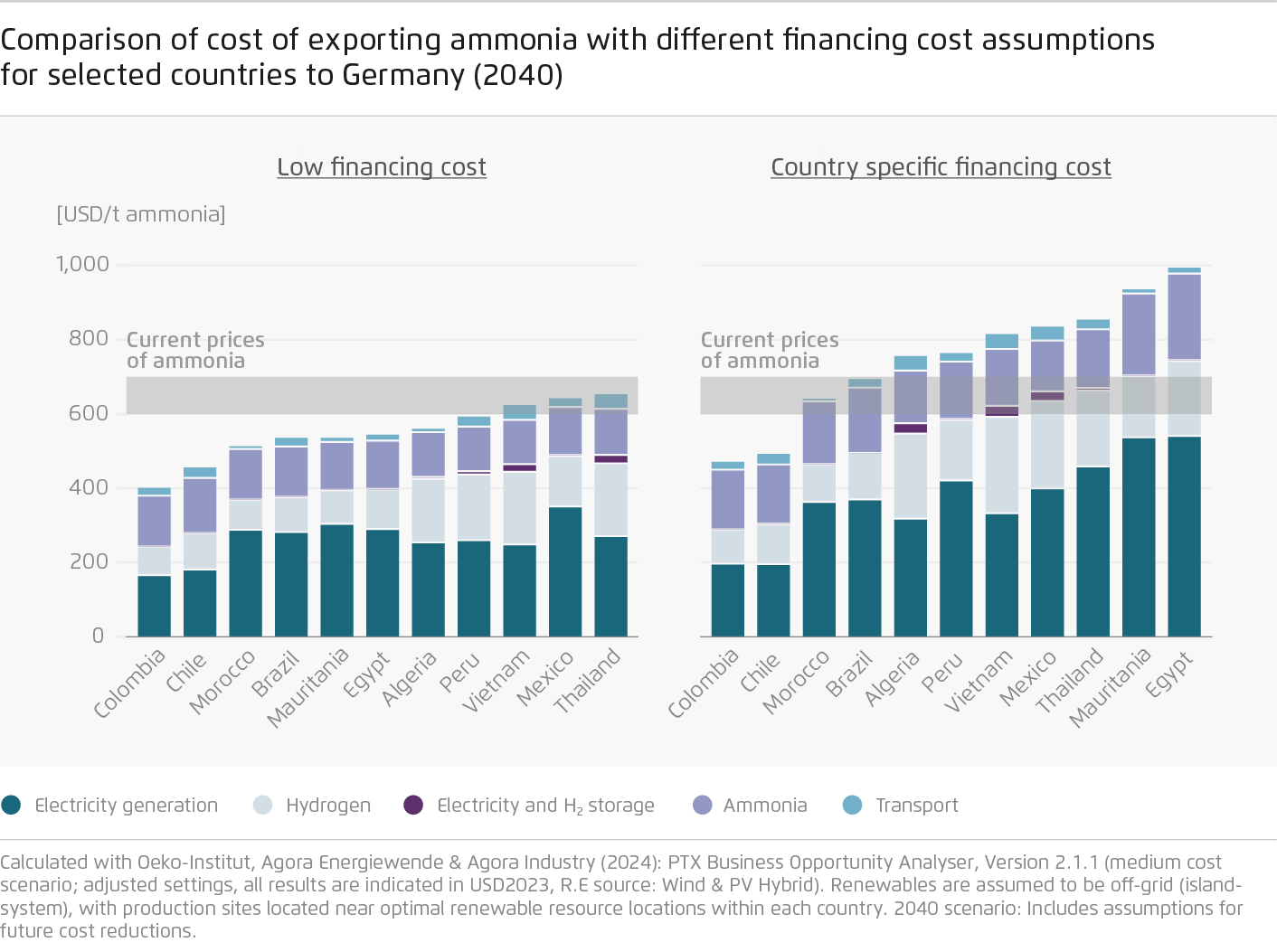

High capital costs and limited access to finance are major barriers to investment in clean alternatives, particularly in emerging and developing economies. Even where renewable resources are abundant, investment is hindered by high perceived risk, demand uncertainty and regulatory and infrastructure constraints. Renewable ammonia illustrates this dynamic: under favourable financing conditions, 2040 export cost projections show that prices in many countries can compete with today’s fossil-based ammonia. However, when country-specific financial risks are factored in, costs skyrocket. This demonstrates that renewable ammonia can be globally competitive, but only if countries have access to affordable, de-risked finance.

Green iron is another promising pathway for value creation in resource-rich countries while enabling a competitive global steel transition – provided that high capital costs are addressed through effective policy and de-risked finance. Our 2025 analysis shows that scaling up green iron production by 2040 could enable countries to significantly boost export revenues, job creation and reduce emissions. For example, 10 million tonnes (Mt) of green iron production in Brazil by 2040 would generate around 35,500 jobs and avoid 12.8 Mt of carbon emissions; South Africa producing 3 Mt could create around 12,000 jobs and avoid roughly 3.8 Mt of emissions.

Building resilience with green alternatives

The global push for green commodities is also a strategic opportunity in an era of geopolitical uncertainty. While conflicts like the war in the Middle East may tempt some fossil fuel producers to double down on production in the short term, they also highlight a critical reality: green energy and commodities enhance resilience and security of supply. Relying on fossil-based inputs in global supply chains creates long-term vulnerabilities, exposing countries to price shocks, supply disruptions and security risks.

Transitioning to green alternatives can mitigate these risks. Fertilisers are a clear example. Today, most are produced using fossil gas, leaving them exposed to market volatility. Green ammonia offers instead a stable, locally producible alternative that can be deployed gradually. And despite concerns that green fertilisers could raise food prices, early procurement evidence suggests only modest impacts: India’s first tender indicated that blending renewable ammonia would increase fertiliser costs by only one to five percent, well within normal market fluctuations.

International mechanisms can accelerate the green transition

Coordinated international action would accelerate the transition by addressing economic, financial and technological barriers simultaneously. Promising approaches are already emerging. The Plans for Accelerating Solutions (PAS) under the COP Action Agenda comprise key initiatives that could be scaled and better aligned, including UNIDO’s Global Clean Hydrogen Programme and the Low-Emission Ammonia-based Fertiliser (LEAF) initiative. Alongside this, country-driven mechanisms – such as the Global Matchmaking Platform and the Industrial Transition Accelerator – facilitate access to finance, technology and technical assistance tailored to national needs. Strengthening alignment across these efforts is critical, as it brings together three central COP priorities: transitioning away from fossil fuels, industrial decarbonisation and climate finance reform.

Stronger cooperation between producer and consumer countries is essential to this approach. Major importers like the EU, China, Japan and India could form demand-side coalitions to create stable markets for green commodities and de-risk investments. In parallel, structured bilateral partnerships with key supplier countries should combine a gradual, predictable phase-down in fossil fuel trade with targeted support for low-carbon industrial development (for example under frameworks like the Equitable Framework and Finance for Extractive‑based Countries in Transition-EFFECT). Priority should be given to countries with limited or newly discovered oil and gas reserves, helping them pivot their investments towards green industries before fossil assets become locked in.

Rather than creating entirely new structures, we recommend that these initiatives could be leveraged under an umbrella “Green Commodities Hub”, a global market-making platform combining concessional and blended finance, guarantees and risk-sharing instruments with technology transfer and stable demand signals. Institutionally, such a hub would rely on coordinated action across stakeholders: governments set the framework and standards, financial institutions offer concessional capital and risk mitigation, and industry drives project development and deployment. Ultimately, this would make low-carbon projects – such as green ammonia and green iron – bankable, accelerating their deployment and unlocking local value creation and jobs.

Tailoring the transition to local realities

No single sector can replace fossil fuel revenues entirely. While renewable hydrogen and its derivatives play an important role, countries need diversified strategies. Building resilient, low-carbon economies will require several complementary pillars such as critical raw materials processing and battery manufacturing to drive a shift away from fossil fuels to renewables-based electrification.

Transition strategies must also reflect country-specific constraints. In energy- or water-constrained-contexts – such as Egypt, Algeria, parts of Chile or Morocco – large-scale production of green commodities may compete with domestic electricity and water needs, requiring careful resource allocation. For renewables-rich areas, decentralised renewable ammonia and nitrogen fertiliser production models also offer a complementary pathway to centralised fertiliser production by improving local access and bypassing infrastructure bottlenecks, particularly in regions currently dependent on fertiliser imports – as shown in our 2025 case studies. By reducing these imports, countries can strengthen supply security and lower their exposure to global price volatilities. One example is Brazil, which today is the world’s largest importer of fertilisers with around 7 Mt of urea and 1.1 Mt of ammonium nitrate imports per year. Renewable electricity needed to produce the fertiliser to meet this demand would be around 40 terawatt hours (assuming 52 kilowatt hours per kilogram hydrogen of electrolyser power consumption). Brazil curtails 33-34 terawatt-hours of wind and solar per year – surplus energy that could power domestic renewable fertiliser production (ONS Dados Abertos).

Now is the time to turn ambition into action. Translating the goal of diversifying away from fossil fuels into real-world investments requires binding regulations, clear policy frameworks and stronger international collaboration, anchored in a global commodities hub and strategic producer-importer partnerships. Over time, these coordinated efforts can reduce fossil fuel dependence by enabling competitive green export sectors, strengthening supply security and advancing climate diplomacy. The upcoming Santa Marta Conference and COP31 in Antalya provide the critical platforms to drive this progress forward.