-

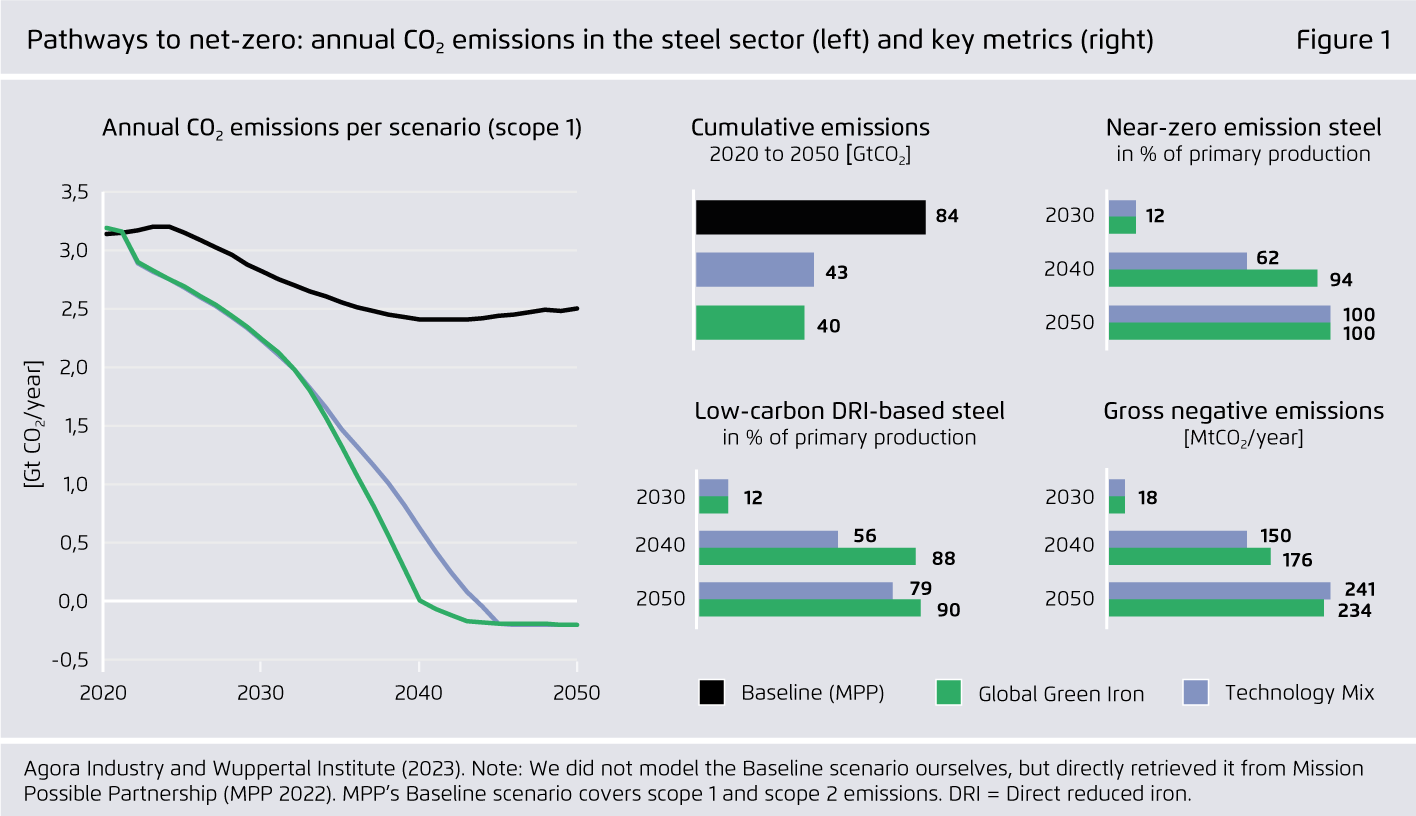

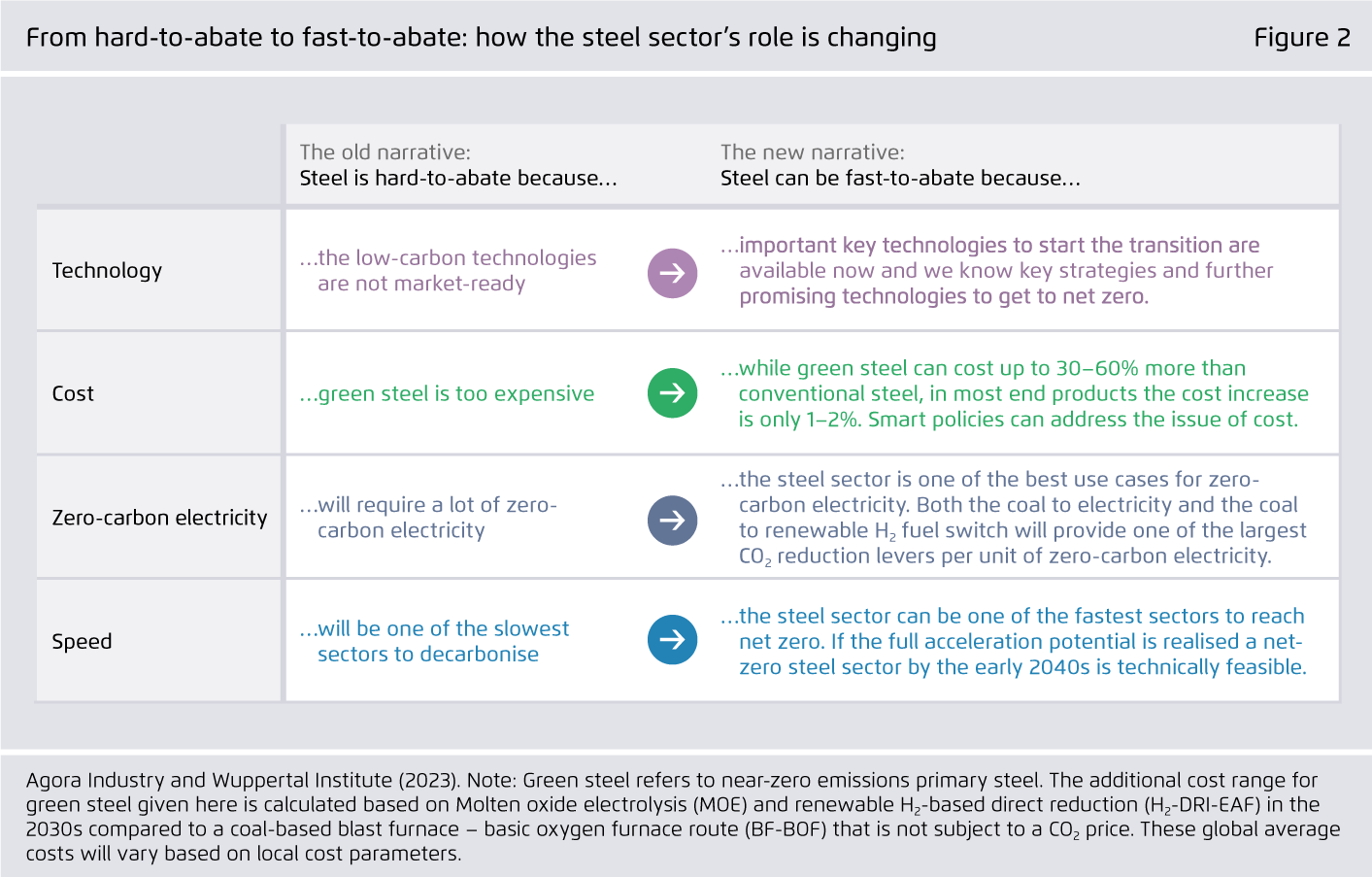

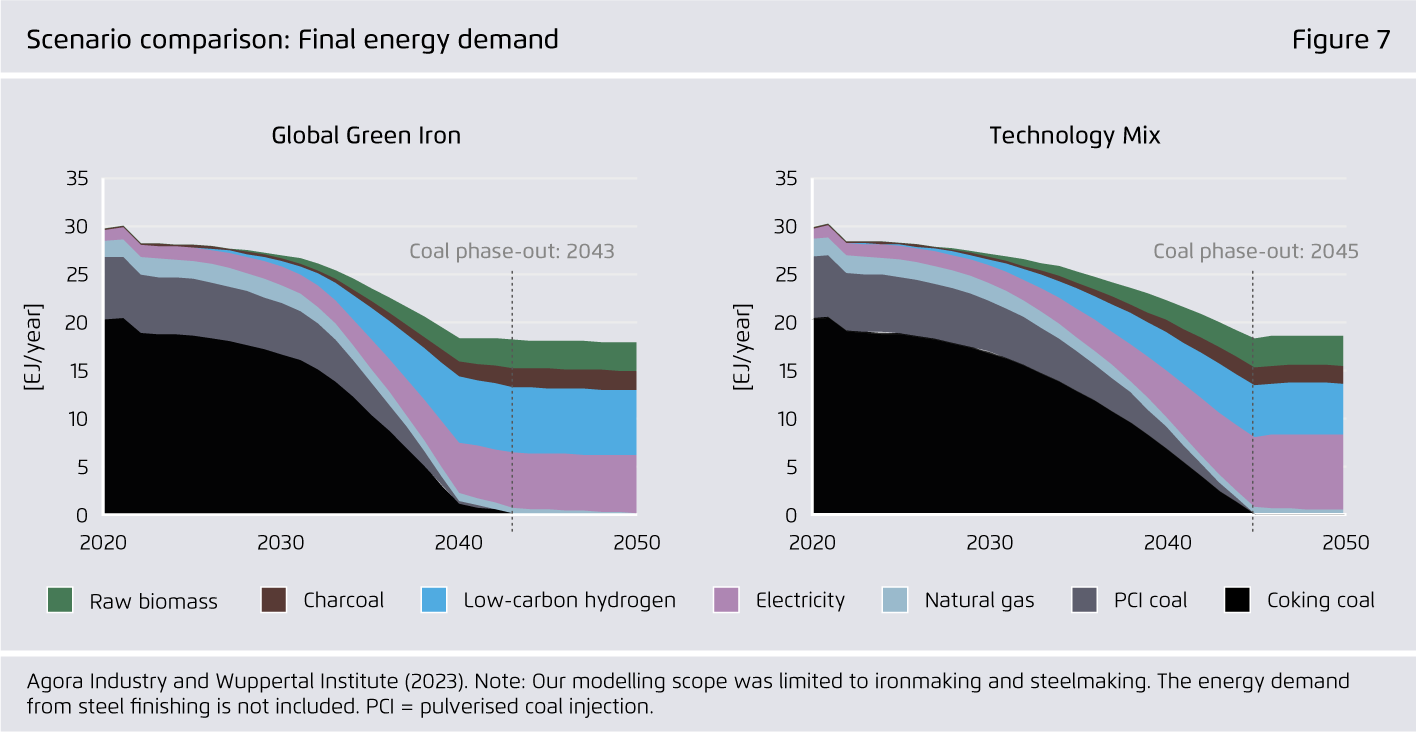

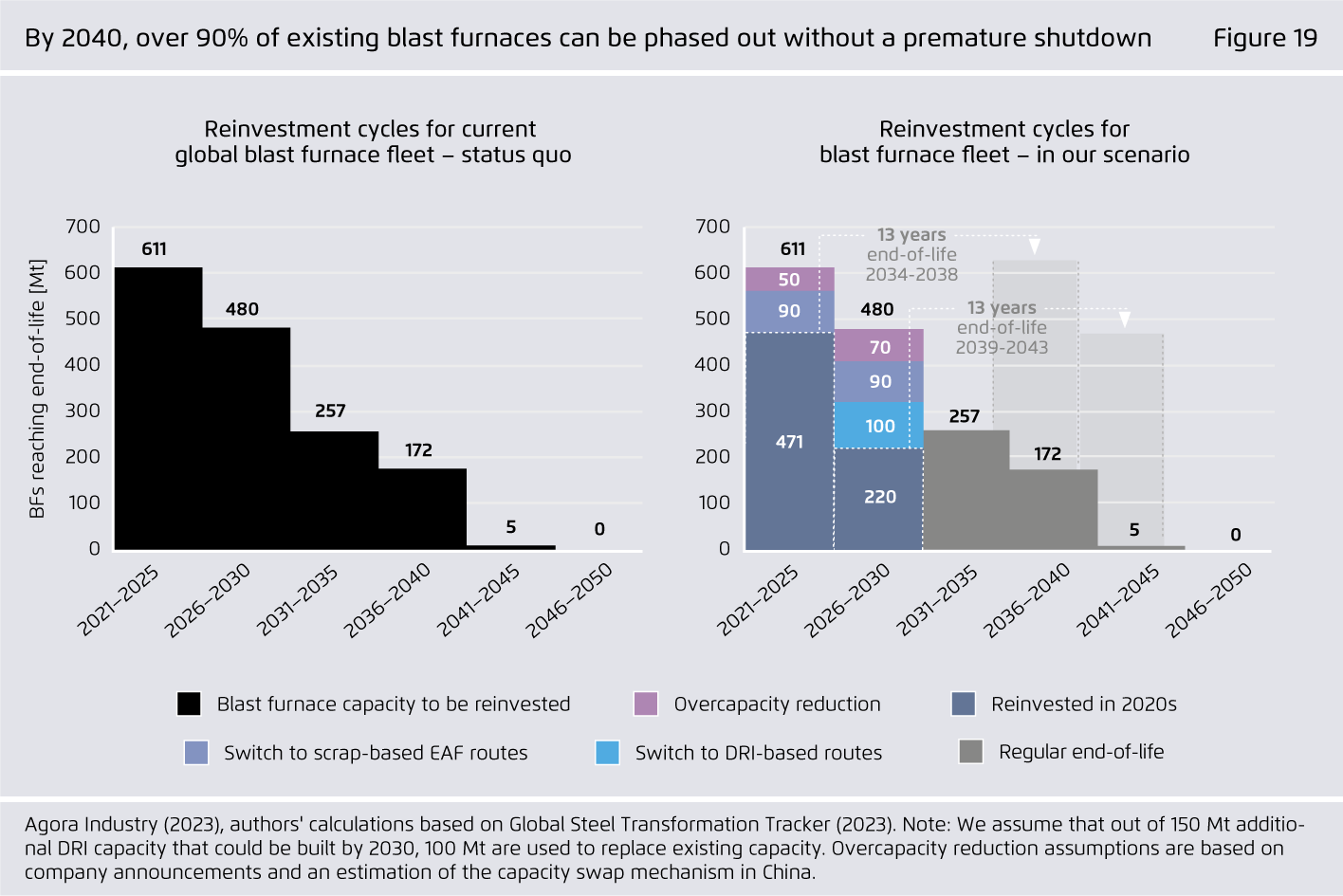

A net-zero steel sector and a coal phase-out in steelmaking by the early 2040s are technically feasible. This can turn iron and steel from a hard-to-abate to a fast-to-abate sector and be a key element to increase global climate ambition.

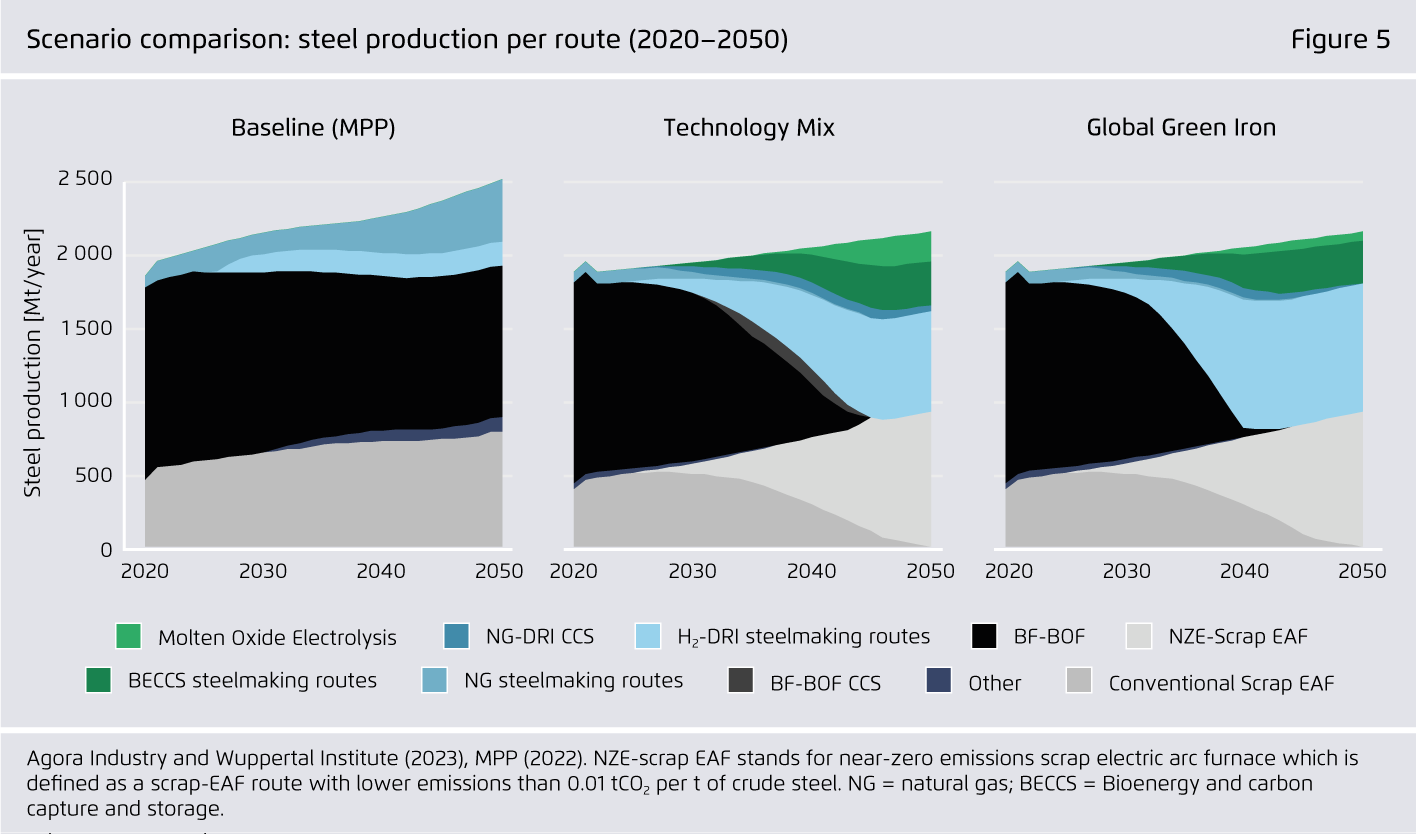

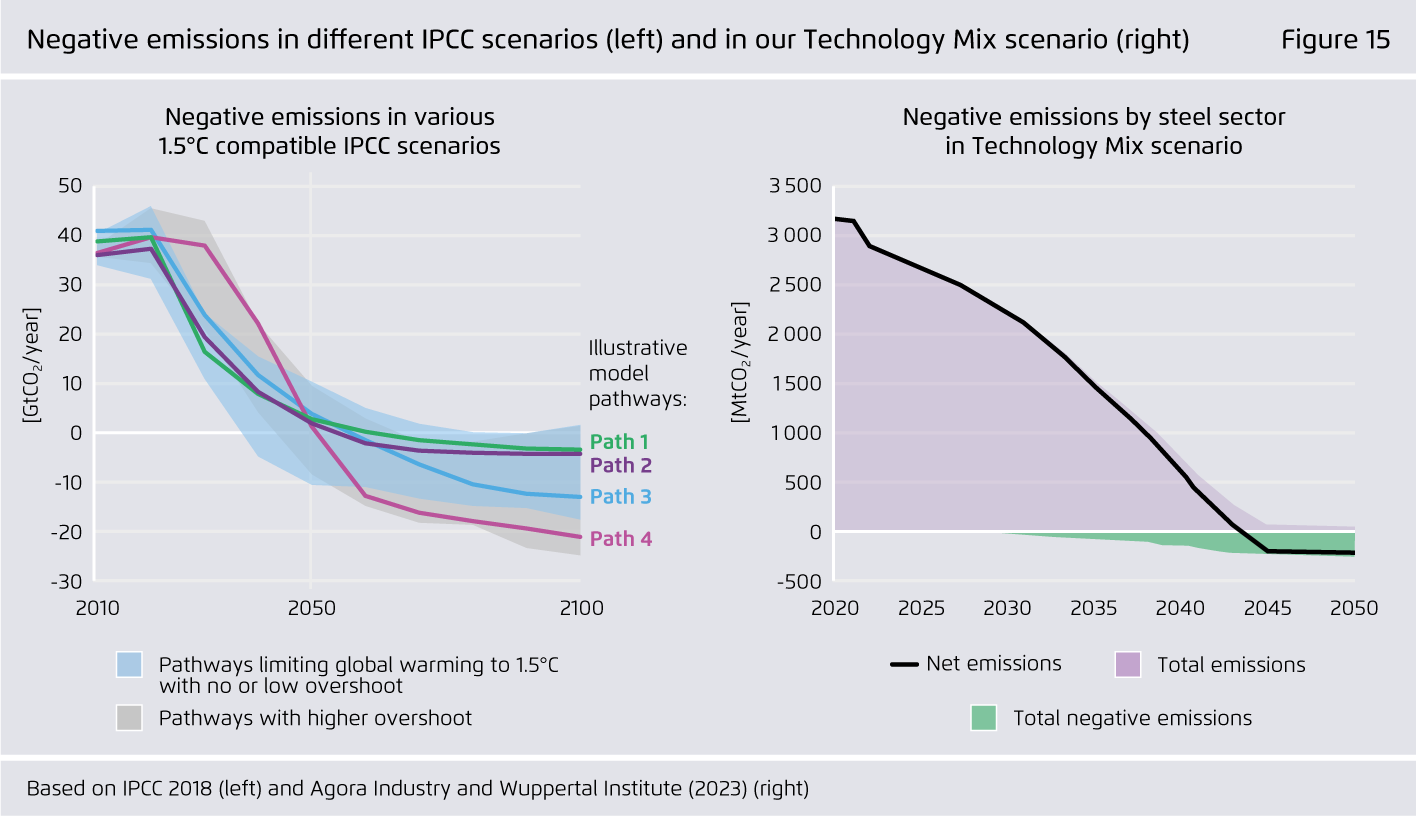

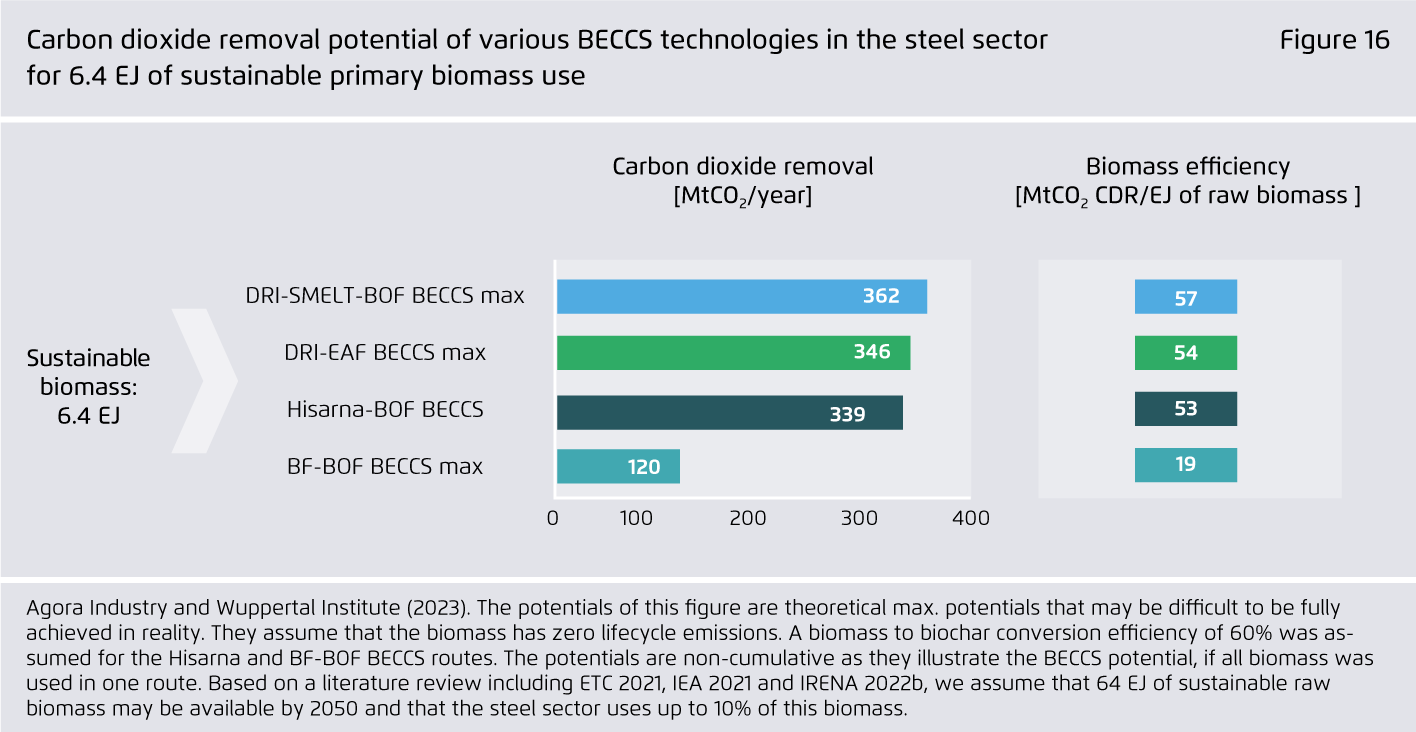

The key strategies to achieve such an accelerated steel transformation are material efficiency, an increase of scrap- and hydrogen-based steelmaking plus bioenergy and carbon capture and storage (BECCS).

-

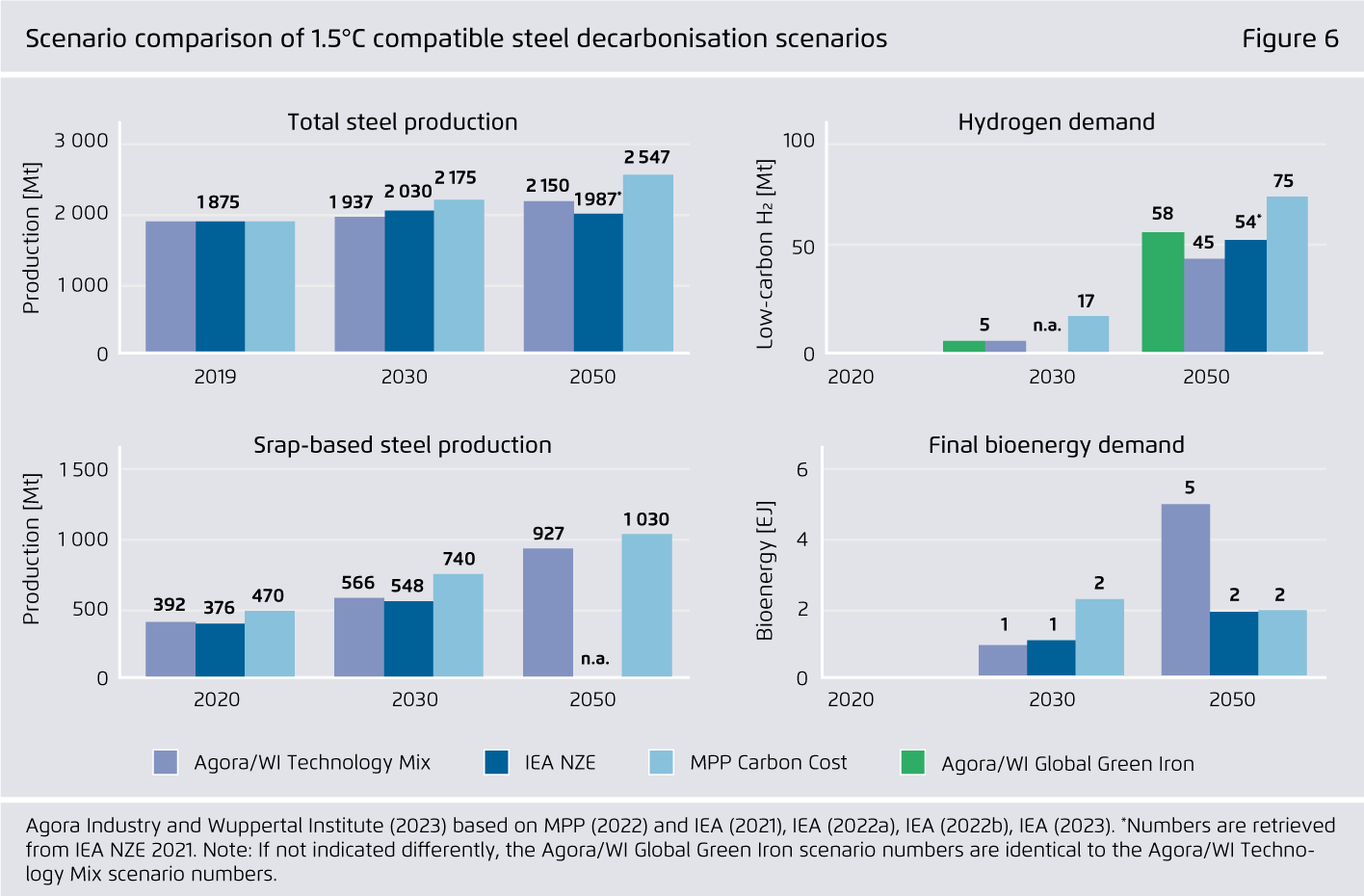

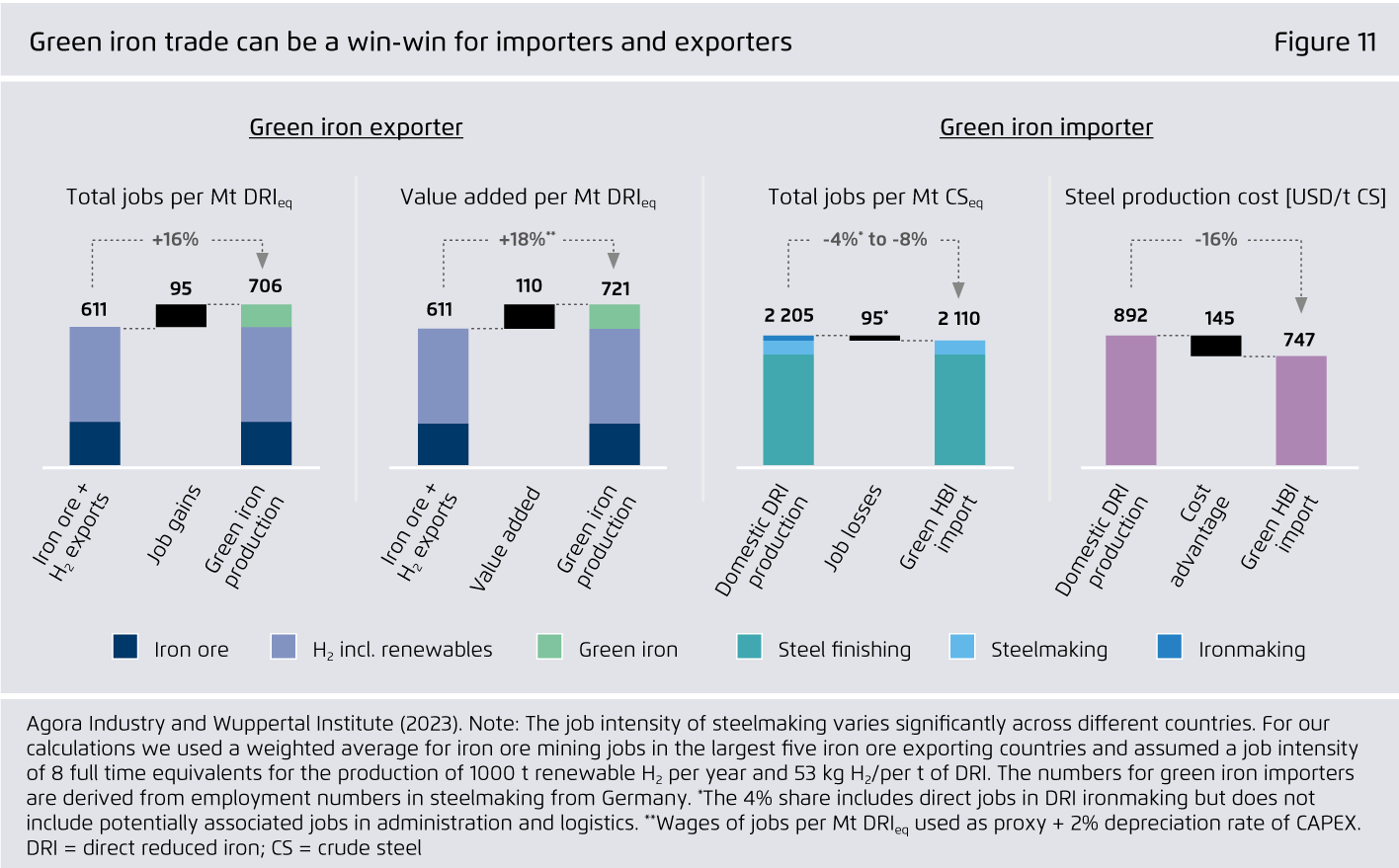

Green iron trade can lower the costs of the global steel transformation and can be a win–win solution for green iron exporters and importers.

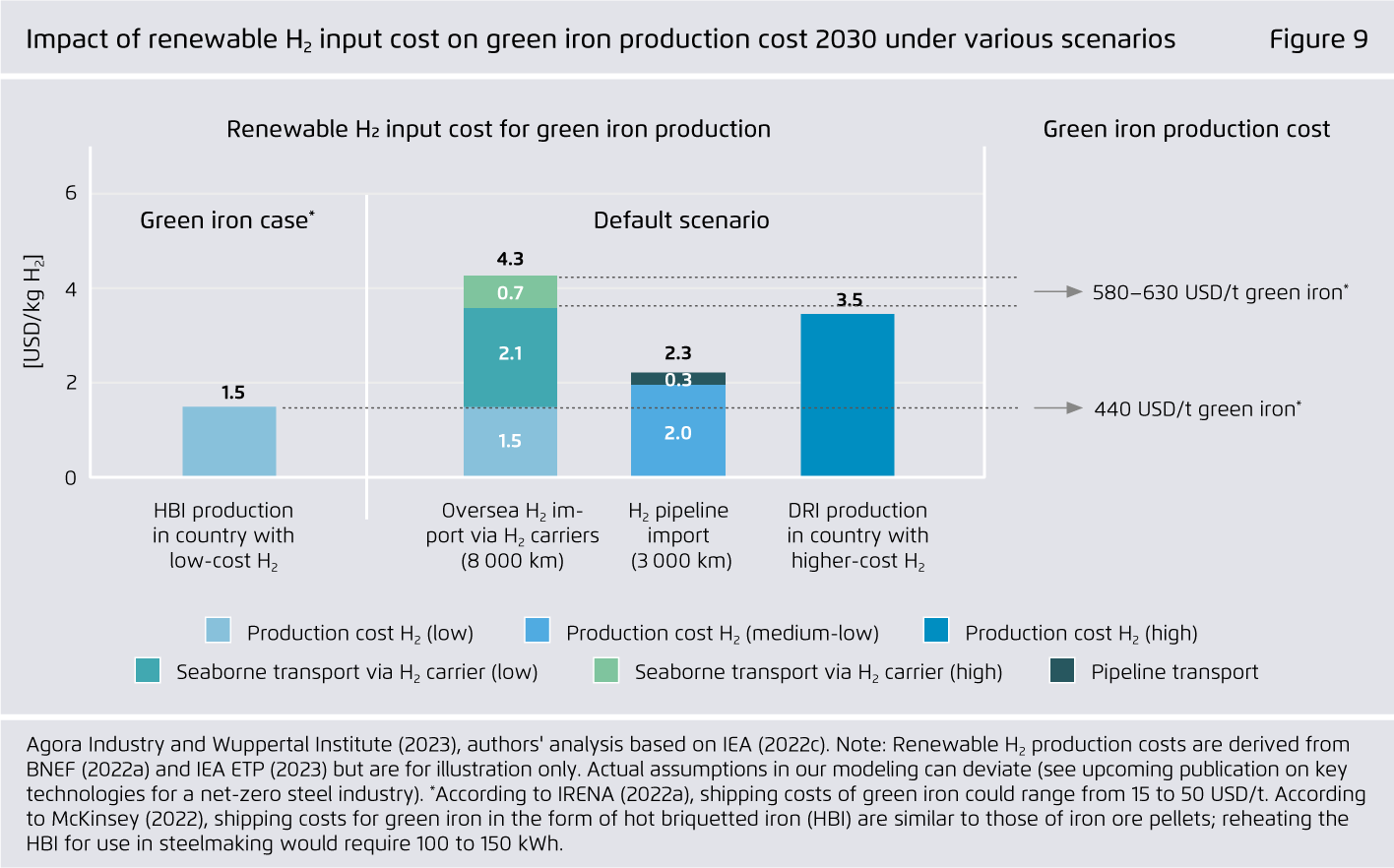

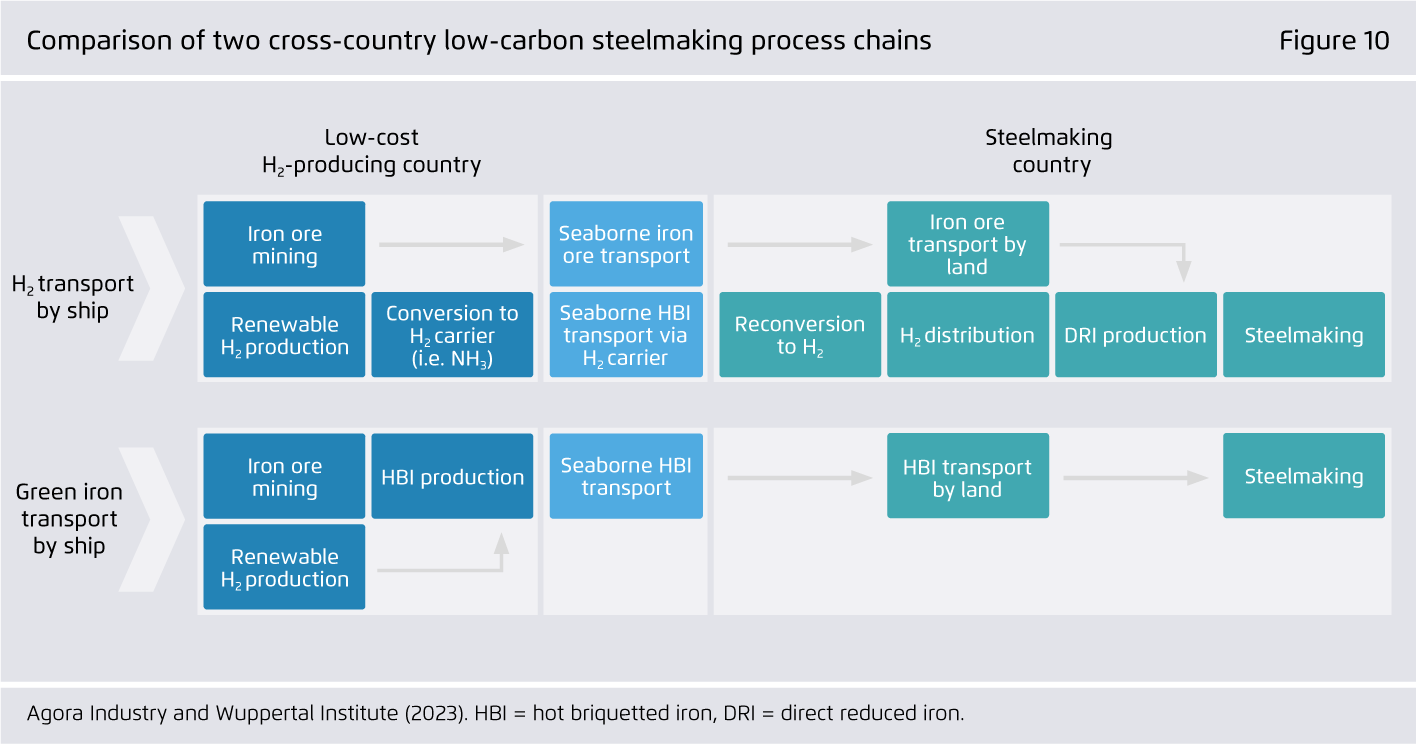

Transporting embodied hydrogen (H₂) as green iron will be significantly cheaper than transporting H₂ and its derivatives by ship. For countries with high renewable H₂ costs, green iron imports can increase the competitiveness of low-carbon steelmaking, thereby helping to safeguard local jobs in the steel industry. For green iron exporters, this can create new jobs and value added.

-

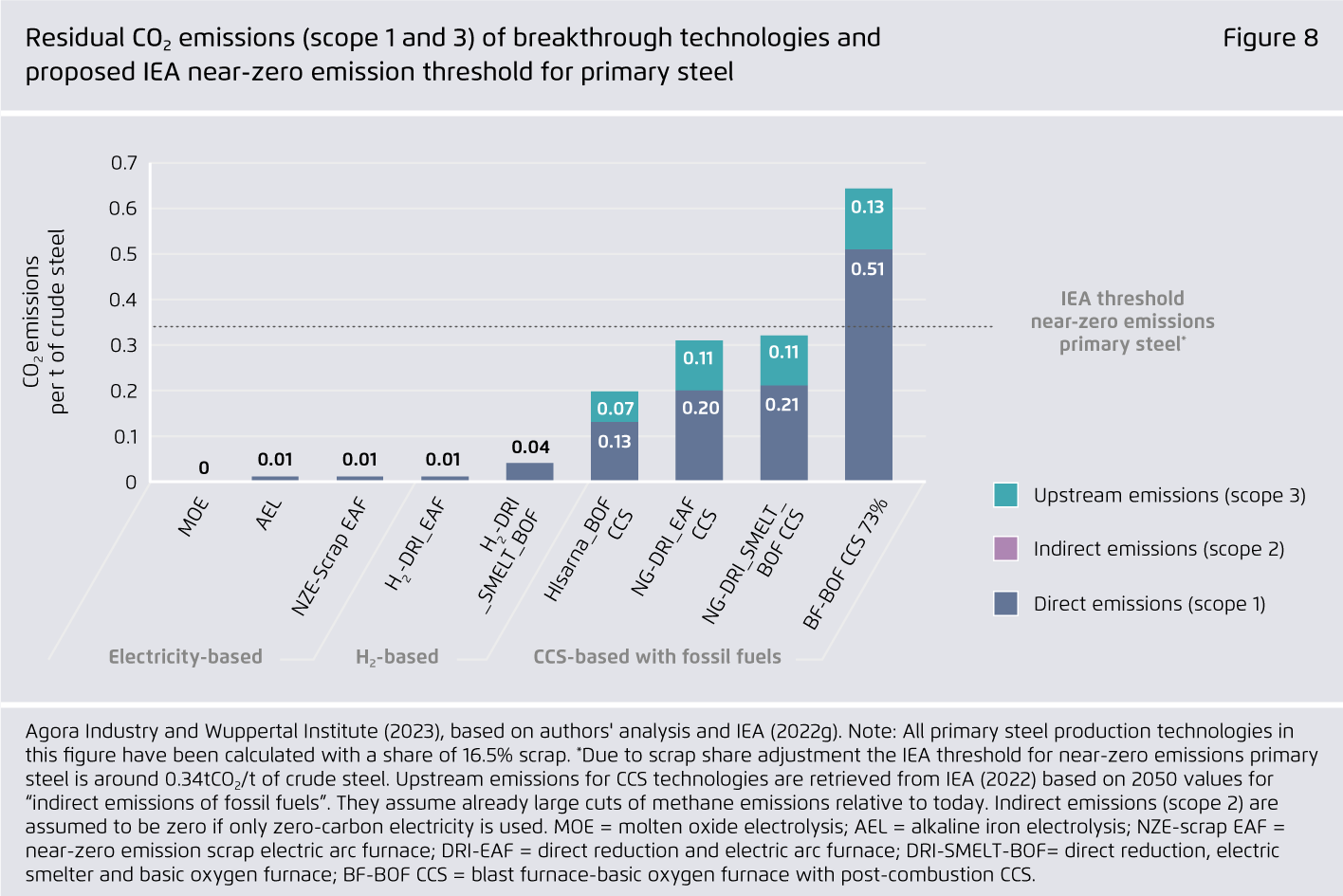

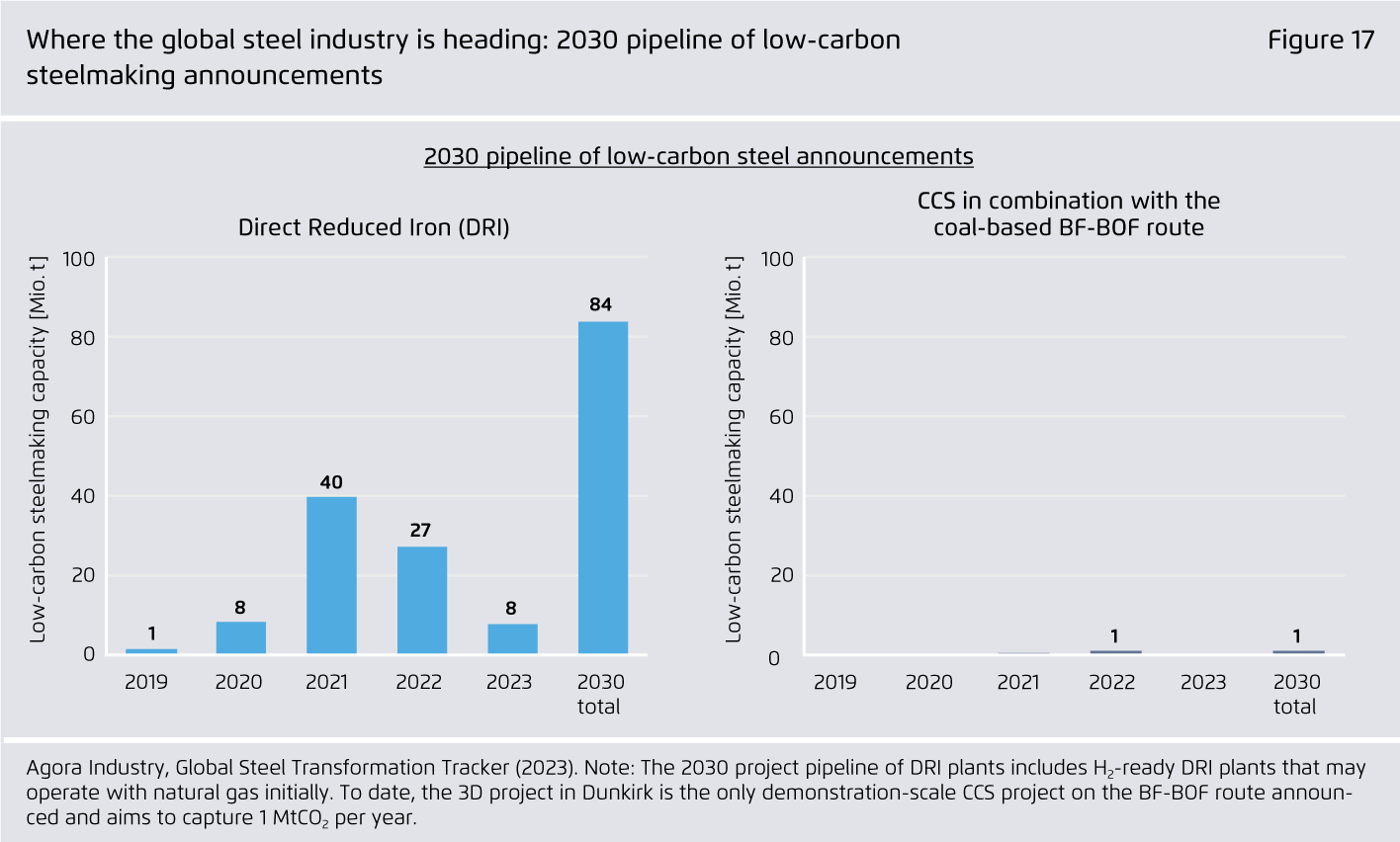

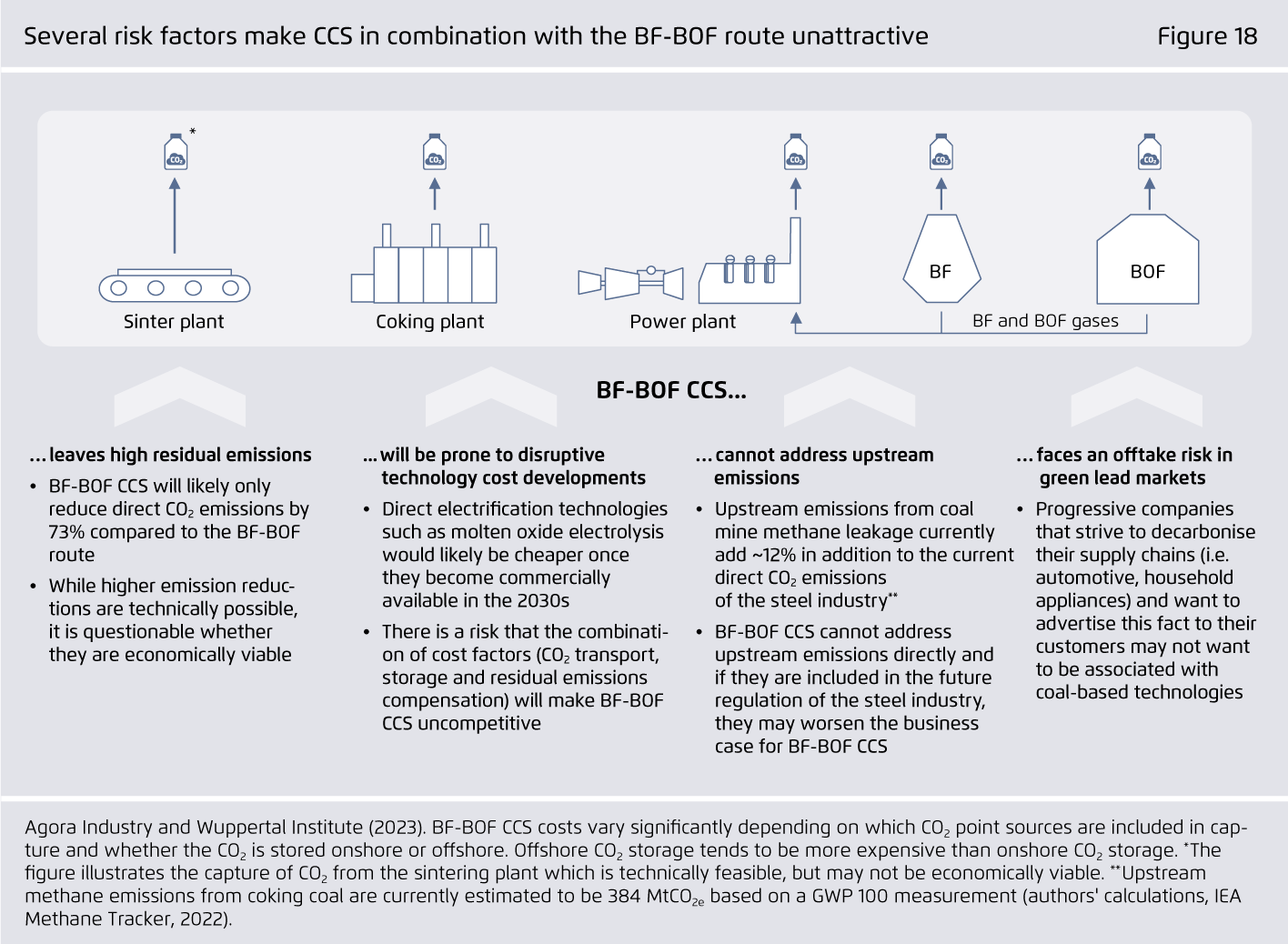

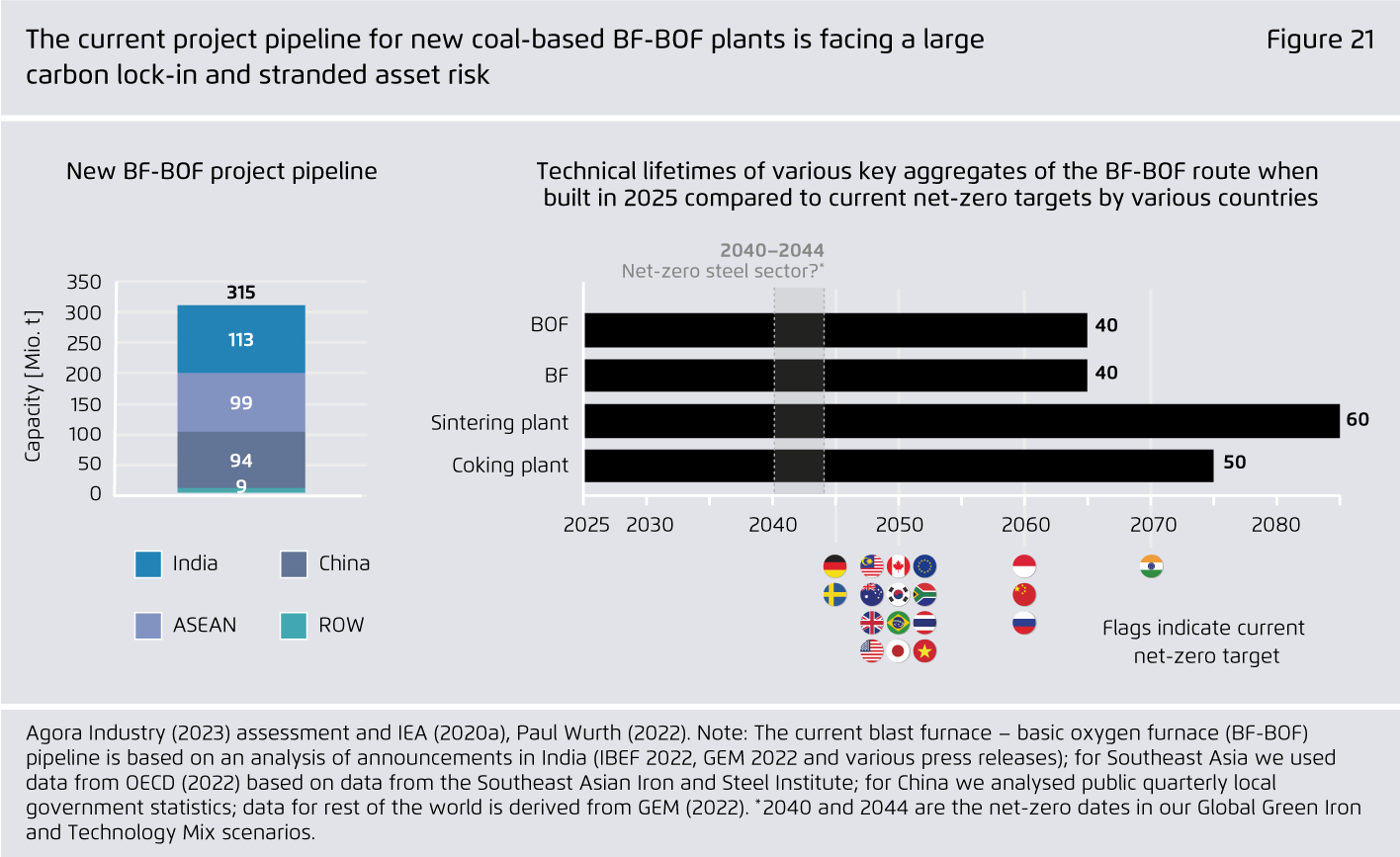

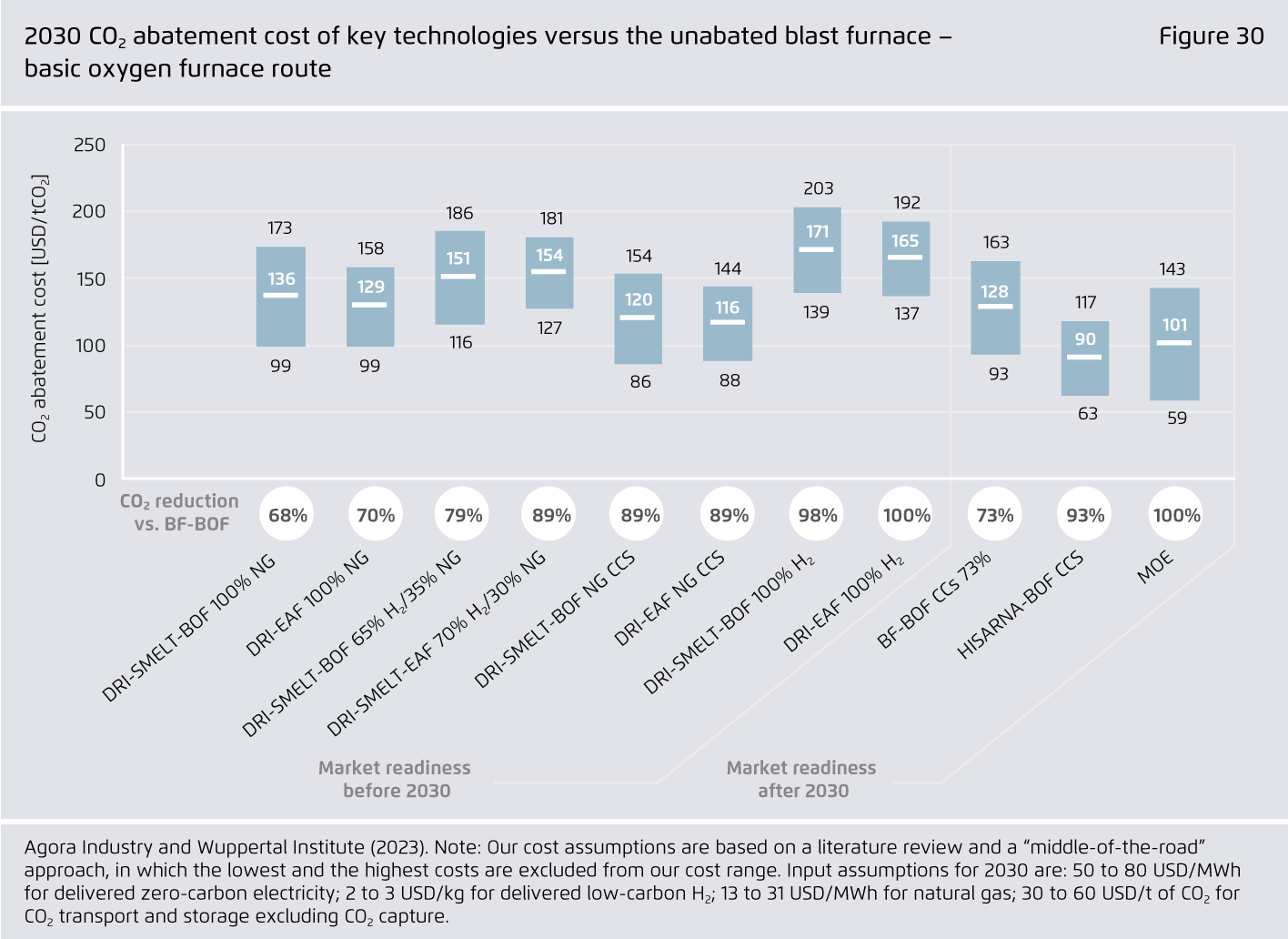

Carbon capture and storage (CCS) on the coal-based blast furnace-basic oxygen furnace route (BF-BOF) will not play an important role in the global steel transformation.

CCS on the BF-BOF route is unlikely to reduce direct CO₂ emissions beyond 73% and cannot address upstream emissions (coal mine methane leakage). Compared to other key technologies, steelmakers’ efforts to commercialise this technology are currently very low. If BF-BOF CCS does not materialise, new coal-based steel plants face a high carbon lock-in and stranded asset risk.

-

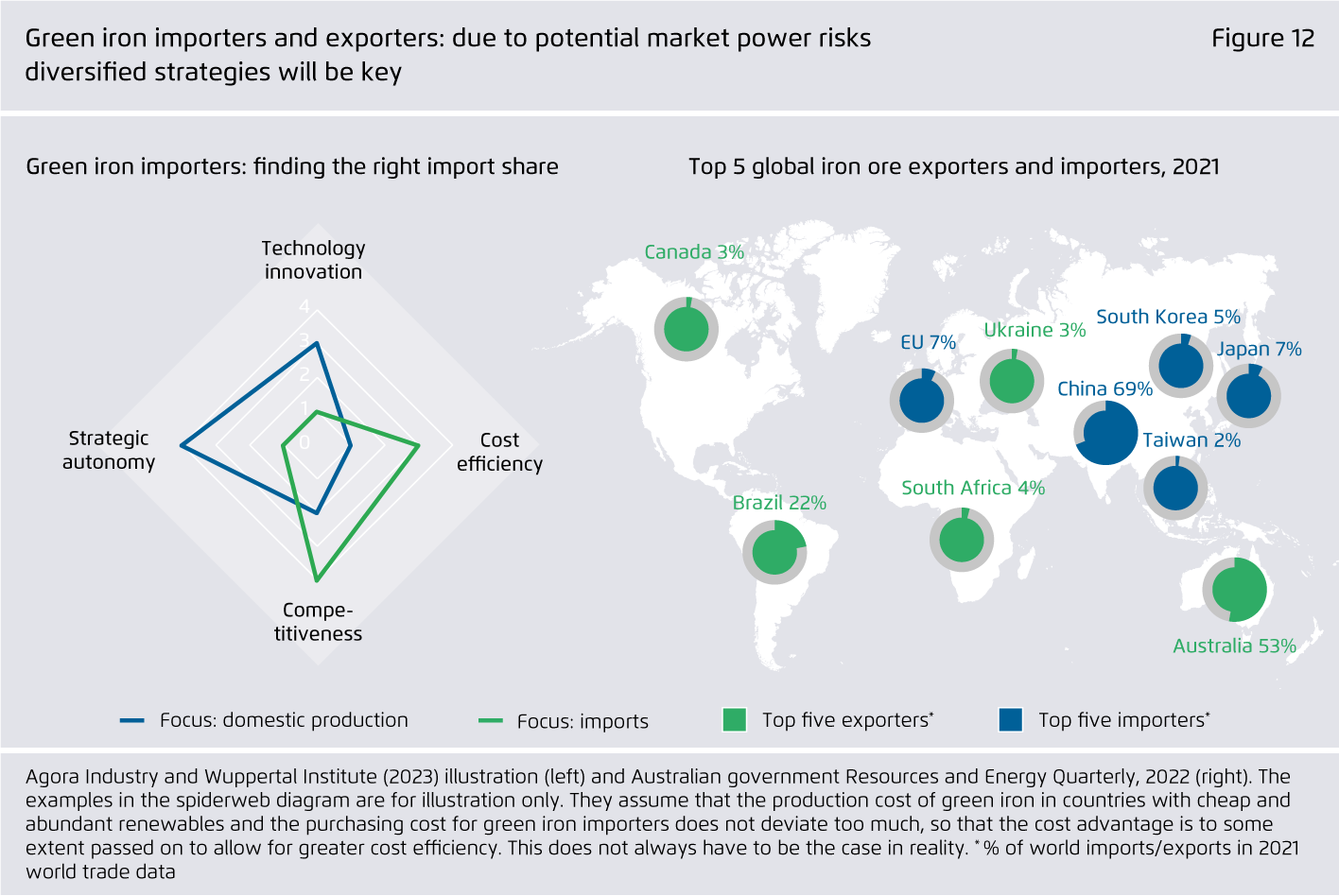

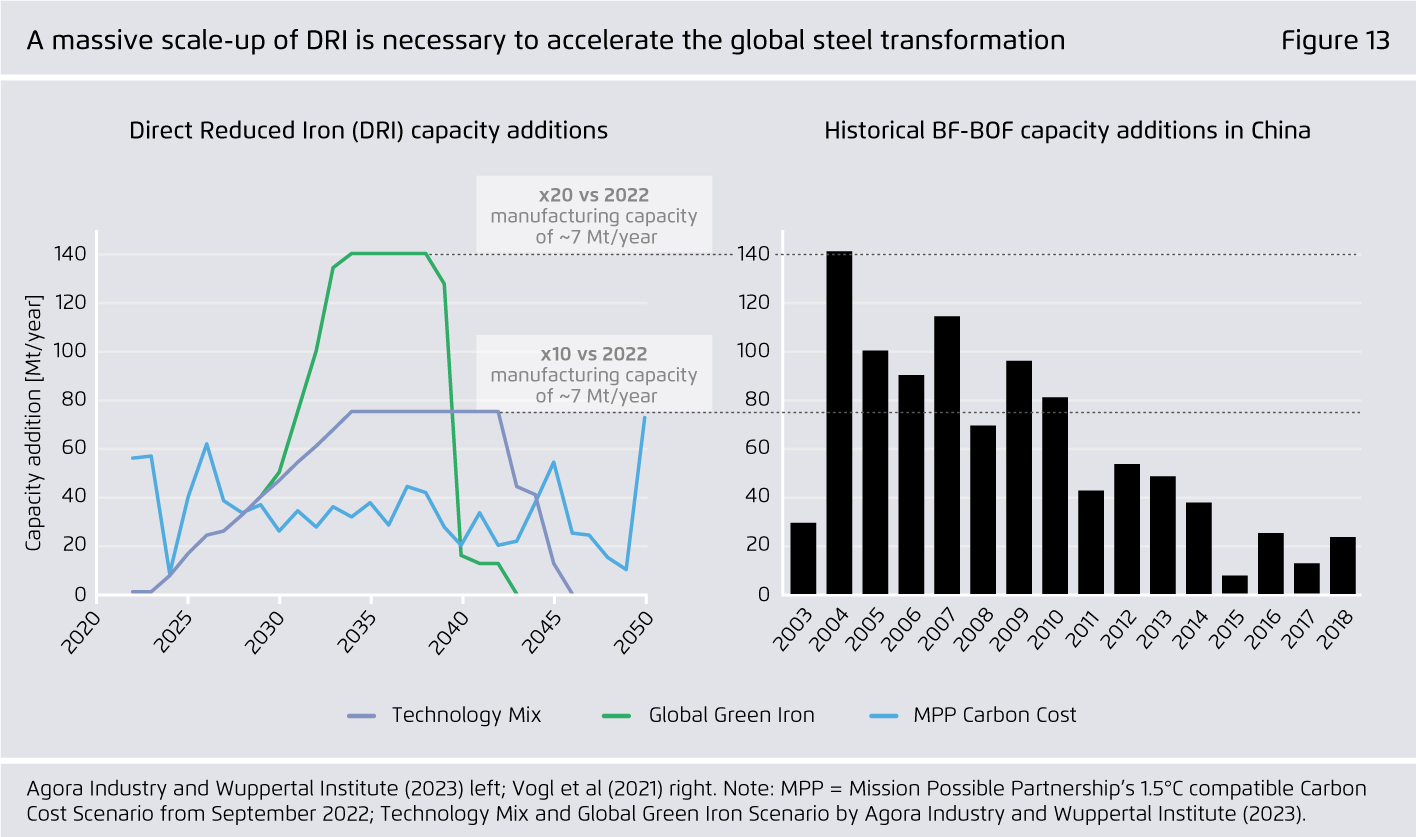

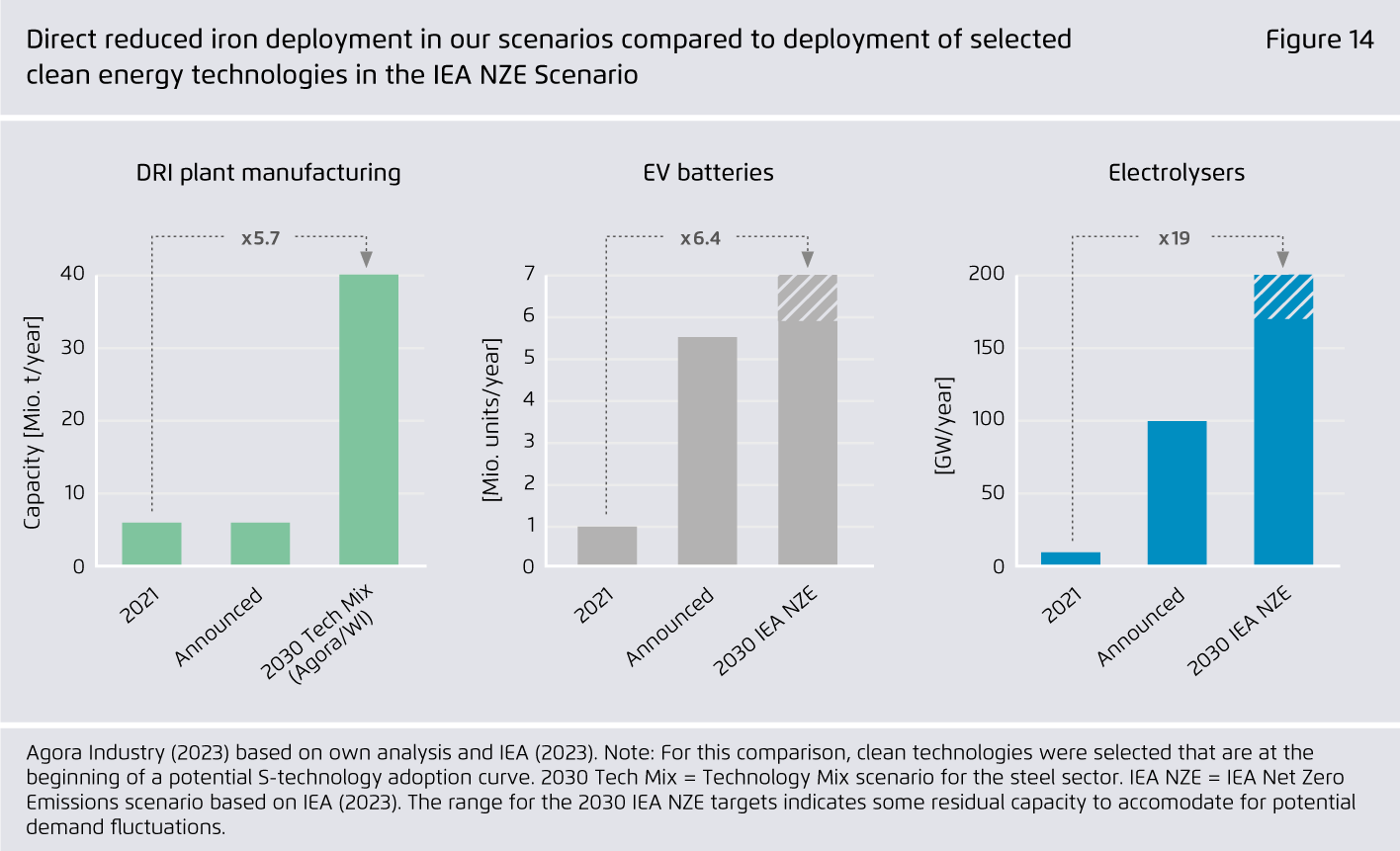

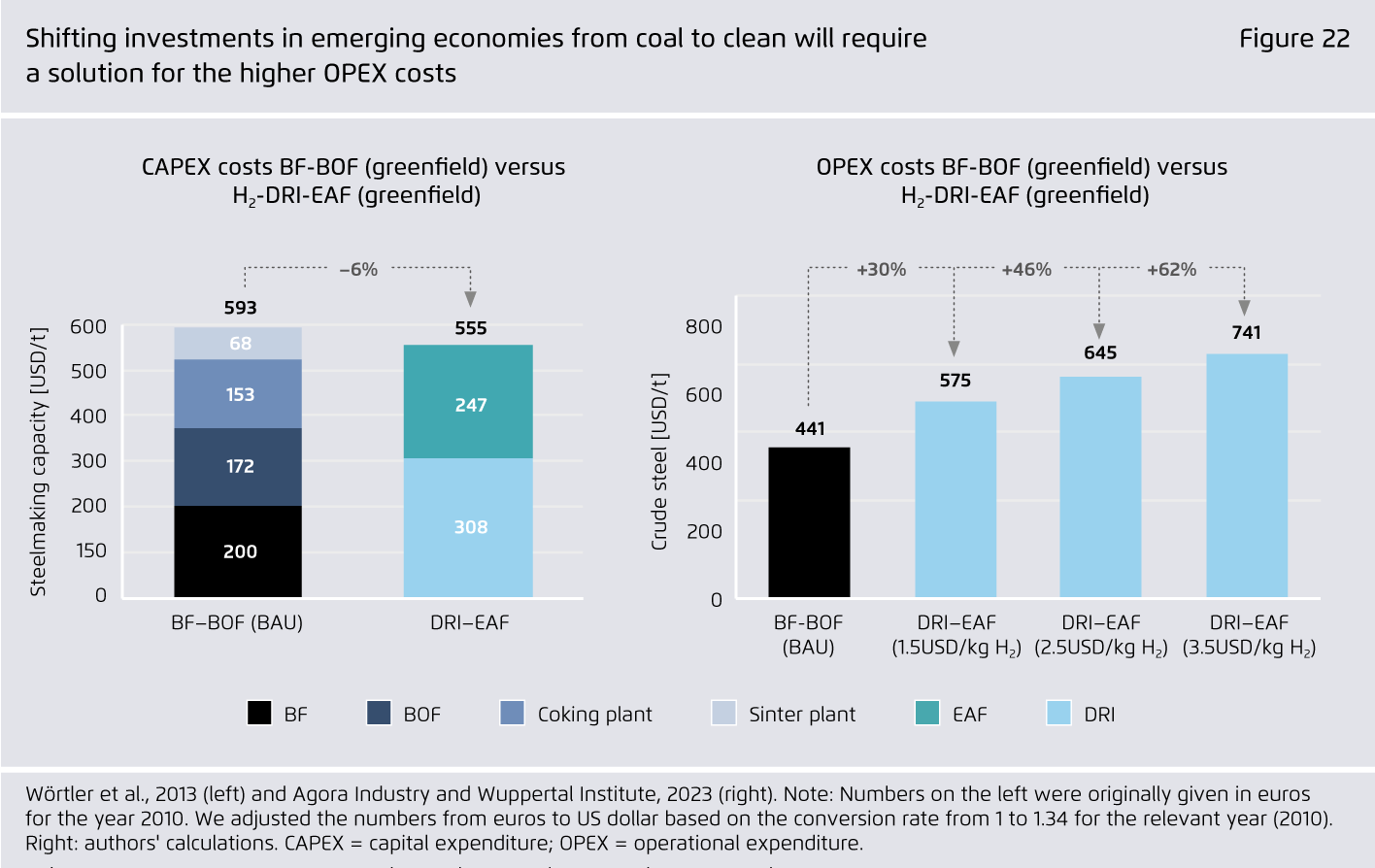

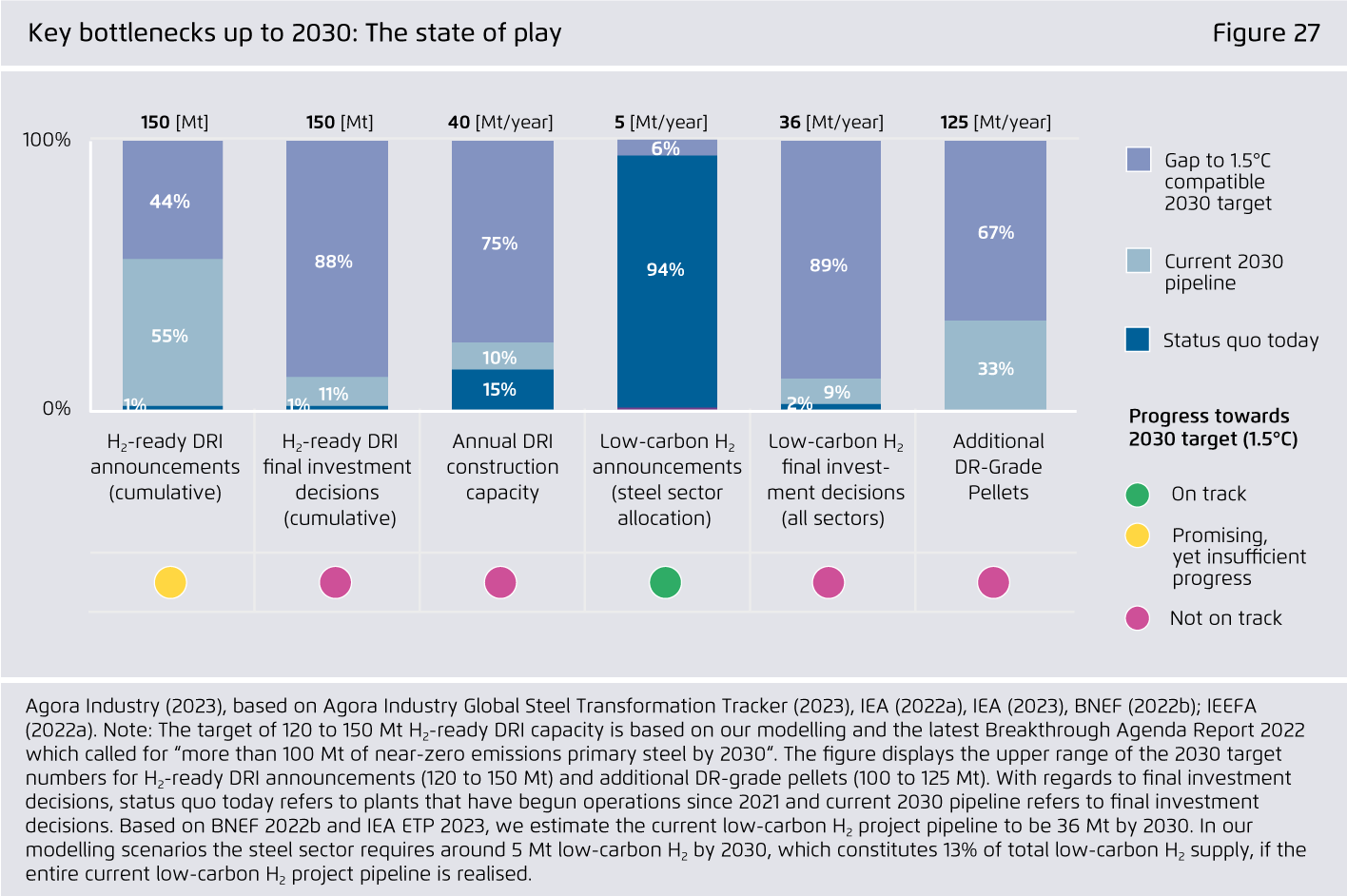

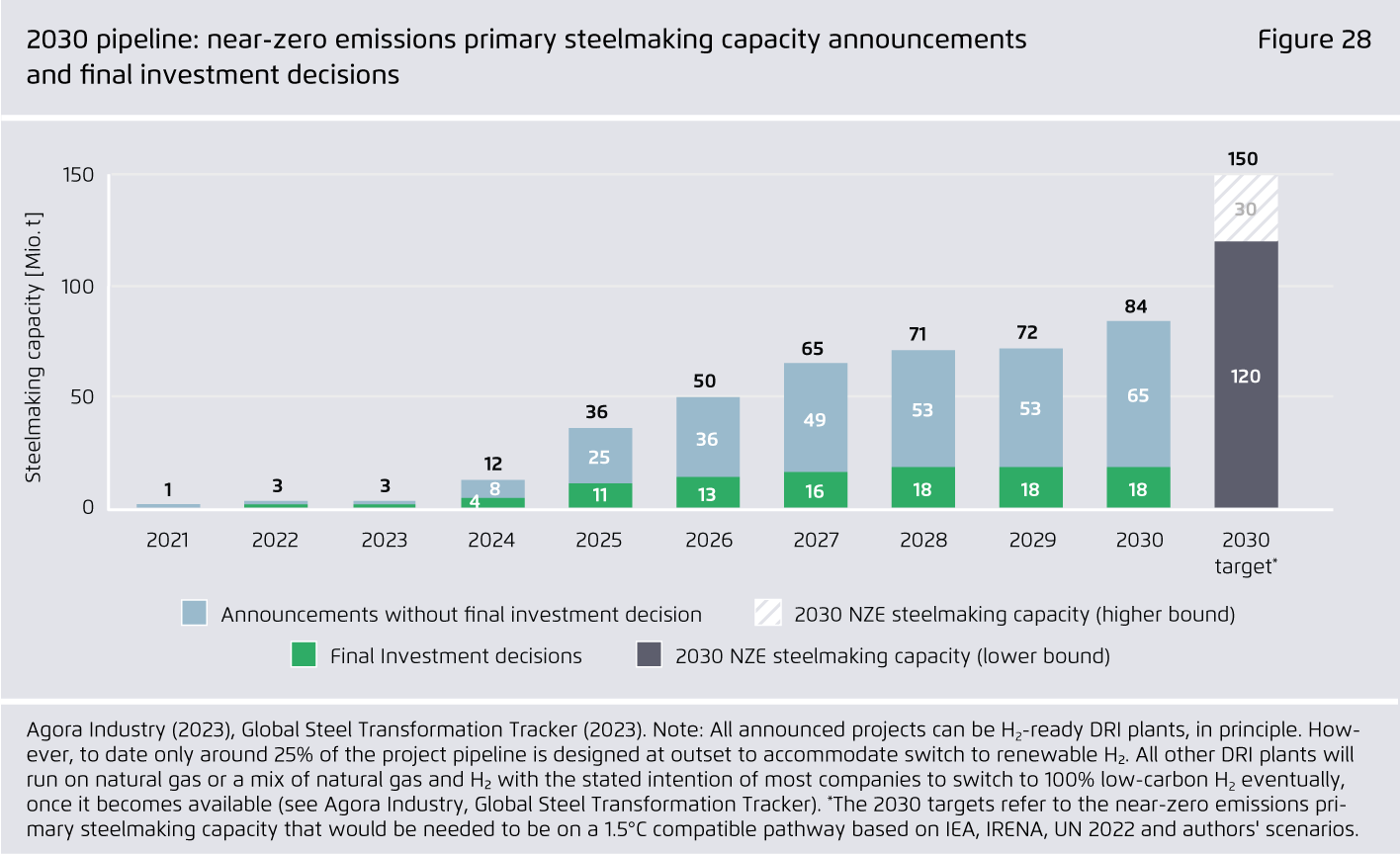

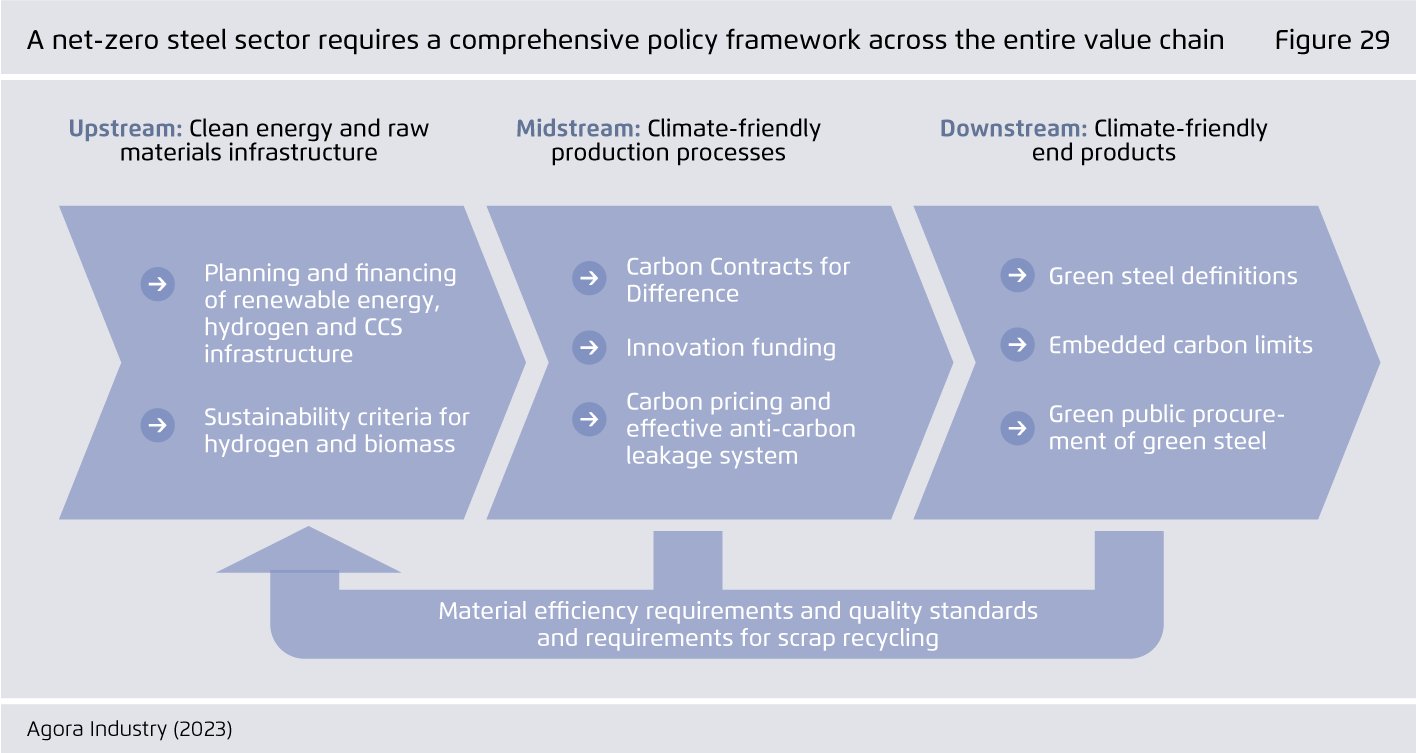

To unlock the full acceleration potential of the steel transformation, national governments need to create an adequate regulatory framework and develop cross-country strategic partnerships.

International cooperation will be needed to address key bottlenecks (i.e. DRI plant engineering, suitable iron ore qualities, low-carbon H₂), minimise stranded assets and help to unlock green iron trade.

-

Related

![[Translate to English:]](/fileadmin/_processed_/8/f/csm_15_insights_global_steel_news_73f640a802.jpg "The global steel industry can achieve net-zero emissions by the early 2040s")

![[Translate to English:]](/fileadmin/_processed_/9/e/csm_global-steel_project_news_2_283e600f74.jpg "Shifting global steel reinvestments from coal to clean")